価値評価の方法

<質問> さきほどマンガーさんが中国市場と米国市場をくらべた話をされていましたが、その際の評価方法としては、株式市場時価総額をGDPで割る方法[バフェット指標]と、CAPEを使う方法[シラーP/E; 景気循環調整後PER]のどちらが適しているとお考えですか。

<バフェット> お話しにあったどちらの基準も、わたしどもが証券の価値を評価する上で最上というわけではありません。将来にわたって事業が稼ぎ得る現金の現在価値は、事業を評価するうえで重要な要因です。しかし世間では絶えず公式を求めていますが、究極の公式というものはありません。なにが変数に関わっているのか、わからないからです。もちろん、それぞれの数値にはそれなりの意味があります。しかし事業の評価とは、「実際に変数の値を完璧に設定できる公式」へと単純化できるものではありません。お話しに挙げられたどちらの数も話題にされることが多いですが、それがとても重要なこともあるでしょうし、無意味同然のこともあると思います。ひとつやふたつの公式で済むほど単純ではありません。

将来の金利がどうなるか、これがいちばん重要です。「取り得る最良のやりかただ」として、現在の利率を当てはめる例がよくあります。30年物債券の利率をみてください。資金を30年間出しておいて、30年後には損も得もなしに無リスクで戻ってほしいと考える人が、どれだけの金利を期待しているかがうかがえるでしょう。その数字について良い予想ができるかと聞かれても何とも申し上げられませんが、だからといって現在の値を使うという意味ではありません。チャーリーのほうも、「お話しに挙げられた2つの基準を物差しにして、中国市場と米国市場を比較評価することはできない」と答えると思います。

<マンガー> 私からは、「釣りをする上での規則その1、魚のいるところで釣れ」と言っただけですよ。腕の良い釣り師にとっては、今なら中国のほうがもっと魚をみつけられるでしょう。私が言ったのはそれだけです。楽しさひとしおの釣場ですよ。

<バフェット> 投資家として事業をもっとうまく評価できるようになりたい方は、ダメな事業をしばらくのあいだ運営する手だてをぜひ見つけるべきです。すぐれた会社に入って失敗させようもない良好な事業から学ぶよりも、ひどい事業に携わって実際に数年間ほど奮闘してみれば、ビジネスについて実にたくさんのことを学べます。わたしどもにとっても、実体験として学んできたことの大きな部分を占めています。良い事業に関わるという意味からすれば、悪い事業に実際に何度か関わって目の当たりにしたことの割合はもっと大きかったと思います。

<マンガー> いや、実にひどいものでしたよ。

<バフェット> どれほどひどいものなのか、どれだけ自分が非力なのか、どれほど優れたIQを以てしても問題を解決できないのか。そういったことも理解できる有意義な経験になると思います。まあ、非常に強くまではお勧めしませんが。

<マンガー> 我々にとっては非常に有益でした。学びたいのであれば、個々人が厳しい経験をするのが一番ですよ。当然ながら我々も、それなりに経験しましたがね。

(PDFファイルのp. 38。Yahoo! Finance映像では5:34:30)

VALUATION METHODS

Q. In looking at the Chinese market vs the U.S. market, what is the best valuation method, market cap divided by GDP or the Cyclically Adjusted P/E (CAPE) method?

Warren Buffett: Both of the standards you mention are not paramount at all in our valuation of securities. The present value of the future cash that can be taken out of the business is the important factor in valuing a business. People are always looking for a formula. There’s not an ultimate formula. You don’t know what to stick in for the variables. Every number has some degree of meaning. Valuation of a business - it is not reducible to any formula where you can actually put in the variables perfectly. Both of the things you mentioned get themselves bandied around a lot. Sometimes they can be very important. Sometimes they can be almost totally unimportant. It’s not quite as simple as having one or two formulas.

The most important thing is future interest rates. People frequently plug in the current interest rate saying that’s the best they can do. The 30-year bond rate should tell you what people who are willing to put out money for 30 years and have no risk of dollar gain or dollar loss at the end of the 30-year period expect to earn. I’m not sure I can come up with a better figure. That doesn’t mean I’m going to use the current figure either. I’d say - I think Charlie’s answer is he does not come up with China vs the US market valuations based on what you’ve mentioned as yardsticks.

Charlie Munger: All I said before is the first rule of fishing is to fish where the fish are. A good fisherman can find more fish in China now. That’s all I meant. It’s a happier hunting ground.

Warren Buffett: If you want to be a good evaluator of businesses, as an investor, you really ought to figure out a way to run a lousy business for awhile. You learn a whole lot more about business by actually struggling with a terrible business for a couple of years than you learn by getting into a very good one where the business is so good you can’t mess it up. It was a big part of our learning experience, and I think a bigger part in the sense of being involved in a good business was actually being involved in some bad businesses and seeing -

Charlie Munger: -how awful it was.

Warren Buffett: How awful it is and how little you can do about it and how IQ does not solve the problem. It’s a useful experience, but I wouldn’t advise too much of it.

Charlie Munger: It was very useful to us. There’s nothing like a personal, painful experience if you want to learn, and we certainly had our share of it.

2017年10月4日水曜日

2017年バークシャー株主総会(7)事業をうまく評価できるようになるには

バークシャー・ハサウェイ年次株主総会の質疑応答から、事業の評価基準に関する話題です。ウォーレン・バフェットからの助言(赤字で強調した箇所)は、おそらく多くの人にとって福音になることと思います。前回分はこちらです。(日本語は拙訳)

2017年8月24日木曜日

2017年バークシャー株主総会(2)EBITDAについて

前回につづいてバークシャー・ハサウェイ年次株主総会の質疑応答から、今回はEBITDAの話題です。(日本語は拙訳)

ウォーレン・バフェットはEBITDAのことを以前から問題視してレターでも取り上げていましたが、映像での発言によれば来年のレターでも触れる予定とのことです(ちなみに今春のレターでは、一言だけの指摘でした)。

人生で後悔したこと及びEBITDAについて

<質問> お二人は、世界中の何百万もの人たちからとても尊敬され、敬愛されていらっしゃいます[上海から来た質問者]。さて質問が2つあります。ひとつめはEBITDA(エビッダー; 利払い税引き償却前利益)についてです。事業を評価するのにふさわしい指標ではないと断言されていますが、なぜでしょうか。ふたつめは、お二人が人生で後悔されたことはありますか。人生や家族、個人的あるいは仕事の上でひとつだけ違うことをしていたら、と思われることは何ですか。

<バフェット> 個人的な問題についてのお返事は期待されないほうがよいかと思います。仕事の話ですと、チャーリー[・マンガー]ともっと早くから出会えていれば、とは何度も話したことがあります。出会った時のわたしは29歳で、彼は35歳でした。それ以降は愉快なことばかりでした。もっと早くから付き合い始めていれば、ずっと楽しかっただろうと思います。実はそうなる機会はありました。同じ商店で働いていたのです。ただし時期がちがっていました。

EBITDAには減価償却費が抜けています。これはもっともタチの悪い支出です。フロートの話題を好んで取り上げますが、フロートとは資金が先に手に入る一方、支出があとになる種類のものです。反対に減価償却費は、フロートとは反対の働きをします。つまり先に資金を支払いますが、会計上の支出はあとになります。これは好ましいものではありません。事業を買う上でほかの条件が同じであれば、減価償却費が発生しないもののほうがずっと望ましいです。固定資産に投じる資金が、基本的には必要ないからです。EBITDAは誤認を招く統計量です。非常に有害な手口で使われる可能性があります。

<マンガー> この問題の恐ろしさや、事業評価に対してその用語をもたらした人々の嫌悪すべき性質について軽くお考えだったように思いますが、どうですかね。まるでリース物件の不動産を扱う仲介業者が、1000平方フィートの一連の部屋をリースしようとする際に、実際は2000平方フィート分だったと言い出すようなものですよ。尊敬に値する行動ではないですね。そのようなやりかたで、かの言葉も広く使われるようになったのです。しかし公正な心を持った人間であれば、減価償却費は費用だと考えますよ。

<バフェット> ウォール街にとっては、とても有益な考えです。

<マンガー> だから連中はそうするのですよ。株価倍率が低くなりますから。

<バフェット> 奇妙なのは、実際にそれが受け入れられた方法です。それはともかく、この用語がどのように使われ、自分たちが使ってみせて概念を売りこむ様子がありありと残されています。2%と20%が同じ種類のものとなるわけです。この用語が通用する間は、この用語で押し通していくでしょう。

<マンガー> 今やビジネス・スクールでも使っています。おぞましくもおぞましいことですよ(笑)。盗人がその用語を使うだけでもうんざりなのに、広まったことでビジネス・スクールも真似をするとなれば、好ましい結末にはならないですね(拍手)。

(PDFファイルのp.45。Yahoo! Finance映像では6:18:40)

REGRETS IN LIFE and EBITDA

Q. You are highly respected and loved by millions globally. You believe EBITDA (is not a good parameter to evaluate a business. Do you have regrets in life, one thing you would have done differently in life, family, personal or business, what is it?

Warren Buffett: I don’t think you should expect us to answer that on personal matters. In business, I’d say I wished I met Charlie earlier. We’ve had a lot of fun ever since I was 29 and he was 35. It would have been even more fun if we started many years earlier. We had a chance to. We worked in the same grocery store but not at the same time.

In respect to EBITDA, it’s the worst kind of expense. We love to talk about float and float is where you get the money first and have the expense later. Depreciation is where you spend the money first and then record the expense later. It’s reverse float. It’s not a good thing. It’s much better to buy a business, everything else being equal, and it has no depreciation because it has essentially no investment in fixed assets. EBITDA is a very misleading statistic that can be used in very pernicious ways.

Charlie Munger: I think you understated the horrors of the subject and the disgusting nature of the people that brought that term when I was in business. It would be like a leasing broker of real estate who has a 1,000 square feet suite to be leased and says there’s 2,000 feet in it - that’s not honorable behavior and that’s the way that term got into common usage. Nobody in his right mind would think depreciation is not an expense.

Warren Buffett: It’s very much in the interest of Wall Street.

Charlie Munger: That’s why they did it. It made the multiple seem lower.

Warren Buffett: What’s amazing is the way it’s accepted actually. It just illustrates how people use language and sell concepts that work to their own use. 2% and 20% has the same sort of thing. As long as it can get sold, it will get sold.

Charlie Munger: Now they use it in the business schools. That is horror-squared. It’s bad enough when the thieves are using the term, but when it gets so common that the business schools copy it, that’s not a good result.

ウォーレン・バフェットはEBITDAのことを以前から問題視してレターでも取り上げていましたが、映像での発言によれば来年のレターでも触れる予定とのことです(ちなみに今春のレターでは、一言だけの指摘でした)。

2015年6月4日木曜日

2015年バークシャー株主総会;すぐれた企業の特徴とは

5月2日に開催されたバークシャー・ハサウェイの年次株主総会から、企業分析についてです。ここでも何度か取りあげているおなじみの話題ですが(参考記事)、うっかりするとおざなりにしてしまう大切なことです。前回分はこちらです。(日本語は拙訳)

<質問> 自信をもって今後10年間の利益を予測できる企業について、特徴が5つあるとすればどんなものがありますか。

<マンガー> 万能のやりかたなど知りませんね。業界というのはそれぞれ違いますから。我々は今も学習し続けています。だから10年前よりはうまくありたいと思いますよ。これだという公式は示せません。

<バフェット> 事業を購入する前にはさまざまな項目を検討します。ほぼそういったフィルターによって、買うのをやめにしています。事業が異なれば、適用するフィルターも非常に異なってきます。ですが5年から10年後にその事業がどうなるのか、それを考えるのに適切な程度は用意するように努めています。いつでも同じ質問が5つということはありません。ただし、「本当にこの事業の経営陣をパートナーにしたいのか」という質問は同じです。その答えが「いいえ」のときは、たとえどんなものでもそれ以上は検討しません。(笑いながら)5つの質問一式などはありません。あったとしてもチャーリーは隠して、わたしには教えてくれませんよ。

A shareholder asked if there were five characteristics of a company that gives one confidence to predict its earnings 10 years out in the future?

Charlie responded, “We don't have a one-size fits all. Every industry is different. We keep learning. What we did 10 years ago, we hope we are doing better now. We can't give you a formula.”

Buffett added that many items are considered before making a purchase. Most of their filters stop them from buying a business. Very different filters apply to different business, but they try to get a reasonable fix on what the business will look like in 5-10 years. It's not the same five questions. However, one question is, “Do we really want to be in a partnership with the management of this business?” If not, that will stop any further consideration. Buffett laughed, “We don't have a list of five. If we do, Charlie has kept it from me.”

2015年5月20日水曜日

2015年バークシャー株主総会;「バフェット指数」について

5月2日に開催されたバークシャー・ハサウェイの年次株主総会から、いわゆる「バフェット指数」の話題です。引用元は前回と同じく、ヘンダーショット女史のメモになります。(拙訳では会話調に変更しています)

<質問9> バフェットさんは以前に、価格水準を評価する基準として、GDP比でみた株式時価総額の割合あるいはGDP比でみた企業利益の割合が高いと言われていました。それでは、現在の市場における評価額は高すぎだと思いますか。(参考記事)

<バフェット> GDPに対する利益水準の割合については、社会のある領域においては問題になるかもしれません。しかし米国のビジネスは、多くの企業が強いられている「ひどく」不利な税率もかかわらず、好調な年がつづいてきました。実のところは、米国企業が見事なほどに発展しつづけてきたからです。もう一方のGDP比での時価総額は、そのときの金利環境に大きく影響されます。現在は米国で極端な低金利になっており、ヨーロッパではマイナス金利です。これは、多くの人がありえないと考えていた状況です。国債の利回りが1%であれば、かつて5%だったときとくらべて[企業]利益はずっと大きな価値があります。機会費用は、実質的に収入の得られない債券を保有するか、株を保有するかのいずれかになるわけです。投資家が株式の価値を見定める際には、金利が信じられないほど低い世界にいるという文脈に立った上で、その低金利がいつまでつづくかを決める必要があります。日本で起きたように何十年も金利が低いままであれば、株価は安いと受けとめられるでしょう。しかし金利が通常の水準まで反転すれば、株価の水準は高いと思われるようになります。

<マンガー> 我々は予想をはずしたわけですよ。ならば、将来どうなるかを我々に訊くのは一体どうしたものですかね。

<バフェット> わたしたちはマクロに基づいて取引を決めません。マクロ要因によって買収をやめた記憶はひとつも思い当たりません。わかっているのは、1年後や2年後にどうなるかわからないことです。しかしバークシャーがよい事業を保有しているのであれば、実のところそれで違いが生じるわけではありません。買収を決める上で考慮にいれる重要な点は、事業がどれだけ強力なmoatを有しており、将来の利益率がどうなっていくのかを判断することです。お抱えのエコノミストが一人いる企業は、従業員が一人余計だと思いますね(笑)。

A shareholder noted that several valuation metrics Buffett has mentioned before such as market capitalization as a percentage of GDP and corporate profits as a percentage of GDP are at high levels. He asked if Buffett thought overall stock market valuations were too high?

While profits/GDP might be a concern for segments of society, Buffett remarked that American business has done well in recent years, despite the "terrible" disadvantage of U.S. tax rates claimed by many companies. The fact is American business has prospered incredibly. The stock market capitalization/GDP is very much affected by the fact we live in an interest rate environment that many would have thought was impossible with extremely low interest rates in the U.S. and negative interest rates in Europe. Profits are worth a whole lot more if the Government bond yield is 1% than if the yield were 5%. The opportunity cost is owning bonds earning practically nothing or stocks. Investors need to look at stock values in the context of a world with incredibly low interest rates and determine how long low interest rates will likely prevail. If interest rates remain low for decades like they did in Japan, stocks will look cheap. If interest rates revert to normal levels, stock valuations would appear high.

Charlie asked, "Since we failed to predict what did happen, why would anyone ask us what our prediction is for the future?"

Buffett said they don't make deals based on macro factors. He can't recall a time ever where Berkshire turned down an acquisition due to macro factors. He said, "We know we don't know what the next 12 or 24 months will look like." It really doesn't make a difference if Berkshire is holding a good business. The important consideration in making acquisitions is determining how strong the competitive moat of the business is and what will be the profitability over time. He joked, "We think any company that has an economist has one employee too many."

2014年10月2日木曜日

2014年バークシャー株主総会; エネルギー事業について

2014年5月に開催されたバークシャー・ハサウェイの年次株主総会から、エネルギー事業(子会社のMidAmerican)への投資に関する話題です。(日本語は拙訳)

備考です。アニュアル・レポートのp.46によれば、バークシャーのエネルギー事業における建造物や機械設備といった減価償却資産の耐用年数は、3-80年間となっています。ちなみに日本の電力会社では、最長で30-50年間のようです(財務省令)。

<質問55> [2013年度アニュアル・レポートの]64ページに載っている事業別の数字ですが、エネルギー事業のEBITDA(利払い税引き償却前利益)から設備投資額を引くと、赤字の営業キャッシュ・フローになります。また直近5年間について同じように計算すると、営業キャッシュ・フローは最高の年で3億ドルでした。これを有形資産額で割ると0.8%のリターンになります。そこまで低いリターンの事業に資本を投じているのはなぜでしょうか。

<バフェット> 有形資産あたりのリターンを出すところまではすばらしいご指摘ですね。投下資本に対するリターンを求める際には、わたしたちも今言われたような計算を好んでやります。資本が正当に使われるのであれば、もっと投じたいと考えています。そうすれば適切なリターンを得られますから。しかしキャッシュ[・フロー]から正味設備投資額を引き算するのではなく、減価償却後の営業利益をみます。正味の設備投資が発生しないときもありますからね。正味投資額が増えざるを得ない領域を好んでいるのは、資本がますます増えますし、規制当局が将来わたしたちを正当に扱ってくれると読んでいるからです。そうなると信じる理由のひとつは、ほとんどの会社が設定しているよりも安い料金で電力を供給する点で、さまざまな他社よりもわたしたちのほうがうまくやってきたからです。アイオワ州にある公益事業では、当社は競合他社よりも大幅に低い料金でやっています。農場をやっている友人は2社から供給を受けていますが、当社の料金は競合よりもびっくりするほど安いと彼は言っています。当局は当社に対して、安全面を含めて相応の敬意を払ってくれています。ですから新しい州で商売を始めると、当局はわたしたちを歓迎してくれます。そういったプロジェクトに新たな資金を投下できれば、良好なリターンが得られると思います。しかし設備投資も含めた上で計算すると、数字としては赤字のリターンになります。この件は鉄道事業とある程度似かよっていますね。

<マンガー> その羅列された数字が落ち目のデパートのものであれば、がっかりですよ。しかし我々は、成長するエネルギー事業に資本を再投資すれば良いリターンが得られる、と自信を持っています。単純なことですよ。

(後略)

Q55: Station 8, New Hampshire. Looking at page 64 segment data for the energy business, when I take ebitda less capex, the result is negative operating cashflow. When I repeat exercise in each of last five years, in best years, $300m of operating cash flow. Divide by tangible assets, 0.8% return, why allocating capital to a business with such low returns?

WB: You were doing great until return on tangible assets. We love the math you describe, as long as we get return on capital investment. We are looking forward to putting more capital in, as long it is treated fairly, and we will get appropriate returns on that. It is not cash minus increased capex, it is operating earnings less depreciation. There are times when no net investment is required, but we prefer where net investment must be higher because we get more capital in and our bet is that regulators will treat us fairly in future. One reason we believe this is true is that we have done so much better than many at delivering electricity at lower rates than charged by most. In Iowa there is a public utility, and our rates are significantly below competitors. A friend with a farm who is served by two utilities tells me that rate from us is dramatically lower than the competitors. We have a deserved good reputation with regulators, including safety. They welcome us when we come to new states. If we can put new money into those projects, we will get good return. But you will get negative returns if you include adding to capital spending. This is somewhat similar at the railroad.

CM: if numbers you recited come from a declining department store, we would hate it. But we have confidence that the reinvested capital will give us a good return from a growing energy business. It is that simple.

備考です。アニュアル・レポートのp.46によれば、バークシャーのエネルギー事業における建造物や機械設備といった減価償却資産の耐用年数は、3-80年間となっています。ちなみに日本の電力会社では、最長で30-50年間のようです(財務省令)。

2014年7月26日土曜日

カミソリに関する豆知識(ウォーレン・バフェット)

ウォーレン・バフェットが1994年にネブラスカ大学でおこなった講演その29で、ジレットの話題です。前回分はこちらです。(日本語は拙訳)

<質問者> 今日のバフェットさんのお話ではバークシャーが保有する銘柄、コークとジレットの2つが登場しました。そういった日用品を扱う別の会社にリグリー[チューインガム]がありますが、バークシャーが同社を購入しないのはなぜでしょうか。どのような理由があればリグリーを購入するのでしょうか。

<バフェット> 銘柄の保有動向のことは触れないようにしています。つまりある銘柄は報告書で開示する義務がありますが、すべての保有状況を示す必要はないわけです。そこには閾値があるのですが、しかし明らかにリグリーは世界規模にわたるフランチャイズを有しています。さて、チューインガムの売上数量の伸びと清涼飲料水の売上数量の伸びをくらべてどう思うか、これがひとつめの疑問点です。それともうひとつ、チューインガムの価格変更のしやすさとコークやジレットをくらべてどうか、これも疑問点です。さらに、その会社の株価をどうとらえるかが大きな要因になると思います。個別の銘柄のことは触れないのでリグリー固有の話はしませんが、しかし世界中で認知されているのは確かです。それはわたしたちの好む種類のものです。

ジレットの話をしますと、彼らは製品をたびたび改良しています。どうか新製品のセンサー・エクセル[替え刃式カミソリ]を買ってみてください。すごくスムーズに剃れますよ。ニューヨーク証券取引所の銘柄コードに使われている「GS」とは、「Good Shave」を意味しています。カミソリ刃の年間販売数は210億本で、ジレットの販売はそのうちの70億本だけですが、価値でみれば60%のシェアを占めています。技術面で進んだ製品を出しているからです。センサーの開発には11年間かかりました。まさに価値ある製品ですよ。ここでおもしろい話をひとつご紹介しましょう。女性用のセンサーはかなりの大型製品になりました。販売開始後の18か月間の売上をくらべると、元々のセンサーよりも女性用センサーのほうがよく売れました。女性の間でカミソリがそこまで広まったのは初めてでした。女性はふつう、使い捨てカミソリか、ご主人やボーイフレンドの替え刃式カミソリを使うものです。しかしある調査結果は興味深いことを示しています(聴衆のみなさんは、いろいろな意味に受けとるでしょう)。男性の場合、カミソリを使っているときに切り傷や擦り傷あるいはどこかを切ってしまうと、カミソリのせいにするものです。しかし女性の場合は自分を責めるのです。そしてその製品は、女性が買いたいと考える種類のものへ加わるわけです。さらに、次のような事実もあります。顔とくらべると脚には、平方センチメートル当たりの感覚器の数がおよそ10分の1しかありません。そのため男性はヒゲ剃りの感触にうるさい傾向があり、女性のほうは脚に切り傷や擦り傷ができるかを気にします。(カミソリにはいろいろな興味ぶかいことがあるのですね)。人類がヒゲを剃り始めたころは石を使っていました。他の人間や動物と戦う際にヒゲがあると不利だったからです。つかみやすいものがあると、敵がつかんでひっぱることで首をへし折られてしまうのですね。この理由は時と共に小さくなりましたが、ヒゲを剃る当初の理由はそうだったのです。

Q. Mr. Buffett, two of the Berkshire holdings that you have were mentioned today, Coke and Gillette. Another company that has repeat daily sales like that is Wrigley. Why has Berkshire not purchased that and what would make you purchase Wrigley?

A. Well, I won't comment on whether we own or don't own anything. I mean there are certain holdings we have to show in our report, but we don't have to show all of our holdings. There are certain threshold levels, but Wrigley is obviously a strong worldwide franchise. How you may feel about the growth in unit sales in chewing gum verses the growth in units sales of soft drinks is one question. How you may feel about the pricing flexibility that they have verses the pricing flexibility that Coke or Gillette may have is another. And then how you feel about the price of a stock in the company would be a major factor. I'm not going to get specific on Wrigley because I don't get specific on stocks. But, it clearly has the kind of worldwide recognition that we like.

In the case of Gillette, they improve the product periodically. I hope you buy a new Sensor Excel because it produces a very smooth shave! The ticker abbreviation used to be "GS" on the New York Stock Exchange, which stood for "good shave". There are about 21 billion blades sold every year. Gillette sells only about 7 billion of them, but they've got about 60% value share because they've done it technologically. The Sensor took 11 years to develop; that is really some product. One thing you'd find interesting: the Sensor for women has become a very big product. More Sensor for women razors were sold in the first 18 months than Sensors were sold originally in their first 18 months. That's the first time a razor's become remotely that popular with women. Normally, women use disposables or they use their husband's or boyfriend's razor. But, one thing research has shown, which is kind of interesting (those of you in the audience will take this several ways). When a man gets a nick or a scrape or cuts himself with a razor, he blames the razor. But when a women does, she blames herself and that enters into the kind of product she wants to buy. It is also true, of course, there's only about one-tenth of the nerve receptors per square centimeter in the leg than there are in the face. So, the man tends to be more sensitive to the feel of the shave, and the women is more sensitive to whether she gets nicks or scrapes on her legs. (There are all kinds of interesting things about razors.) People originally started shaving with rocks because it was a disadvantage in combat with other humans or animals to have something the enemy could grab you by and snap your neck with. That's diminished over the years, but that was the original reason.

2014年5月14日水曜日

2014年バークシャー株主総会;資本コストについて

2014年5月に開催されたバークシャー・ハサウェイの年次株主総会、質疑応答のメモの決定版と思われるものが出始めました。以下のリンク先がそれです。今回はそのメモから資本コストの話題を引用します。ただし前回ご紹介したメモの内容と照らし合わせた上で、訳文を適宜補正しています。(日本語は拙訳)

Notes from the 2014 Berkshire Hathaway Annual Meeting (著者:Peter Boodell氏他、掲載サイト:Scribd)

ウォーレンはさりげなく示していますが、この会話に登場するもうひとつの大切なことは、個人的には「テコ」だと感じました。

Notes from the 2014 Berkshire Hathaway Annual Meeting (著者:Peter Boodell氏他、掲載サイト:Scribd)

<質問8> 並外れたリターンをあげる能力によって経営陣の良しあしの度合いがわかると思いますが、会社の規模が大きすぎるともなれば、それはむずかしくなると思います。巨額の設備投資が必要な会社が[子会社として]新たに加わったことで、資本コストはどうなりましたか。

<バフェット> 規模の大きさが業績の足かせになるのは言うまでもありません。それが本当に足を引っ張るところまでわたしたちは進んで、そのことを確かめてみるつもりです。市場価値が3,000億ドルもの資本となると、以前と同じリターンはあげられません。たしかアルキメデスは十分に長いテコがあれば世界を動かせると言ってましたよね。わたしにもそのテコがあればと思います。さて2つの質問に答えますと、資本コストとは何かですが、わたしたちが2番目に優れていると考えるアイデアが生み出すものだと思います。そしていちばんのアイデアとは、それを超えるものを指します。どうやれば資本コストを決められるかは、過去に何度も議論されてきましたが...。

<マンガー> まともなものは、ひとつも聞いたことがないですね。

<バフェット> わたしたちにもわかりませんが、[投資先の企業が]わたしの良しとしない考えであっても賛成票を投じるつもりです。少しは例外があると思いますが[コカ・コーラ社の議決権行使を棄権した最近の話題に引っかけている]。長期的な観点で[資本効率を]まさに確かめるには、留保した資本1ドルが1ドル超の市場価値を生み出しているかをみればよいと思います。何十億ドルと投下したコスト以上に増えていけば、わたしたちはそのままつづけていきます。あるカナダの企業に30億ドル近くの資本を投下しましたが、きっと成功するでしょうし、当時は30億ドルでその投資をするのが最良の選択でした。ところで、CEOが実行したがっている案件に対して「それは資本コストを超えられません」とCFOが反対するような例は、一度も目にしたことがありません。一方わたしたちは事業を評価できると考えていますし、当社の資本の状況もわかっています。資本コストは重要な課題なので、継続的に見定めています。

<マンガー> 「資本コスト」という言いかたを我々はしませんね。ウォーレンの言うところの、つまり「投下した以上に市場価値を増やす」とする定義は、ビジネススクールでは決して教えないでしょう。「留保したものによって、いっそうの価値を生み出す」、これこそ最良の表現です。我々が正しく、連中がまちがっている。それだけですよ。

<バフェット> ほら、彼よりもわたしのほうがまともに見えるでしょう(笑)。(p.5)

Q8: Gregory Warren, Morningstar (GW): The measure of a good management is ability to generate outsized returns, but sheer size makes it hard. What is cost of capital now, with new capex‐heavy firms?

WB: There is no question that size is an anchor to performance. We intend to prove that up to the point it starts really biting. We can't have same returns on capital base, market cap of $300bil. Archimedes, didn't he say he could move the world if he had a long enough lever, and wish I had that lever. We'll answer two questions. Cost of capital is what can be produced by our second best idea. Our best idea has to exceed that. We've heard so many discussions on how to figure out the cost of capital…

CM: I've never heard an intelligent one.

WB: We don't know, I probably vote if I don't like it but some exceptions to that. The real test over time is that the capital we retain produces more than a dollar of market value over time. If we keep putting billions in, and adding more than their cost, we'll keep doing it. We are spending close to $3bil on a Canadian company, and we will be better off and that was best thing to do that day with that $3bil. I've never seen a CEO wanting to do a deal and a CFO say it didn't exceed cost of capital. We think we can evaluate businesses, we know our capital. We are constantly measuring that opportunity cost, it is an important subject.

CM: A phrase like "cost of capital" we just don't use it. Warren's definition of adding more in market value than we put in will never be taught in business school - the phrase to retain to create more value, is the best description. It's simple: we're right, and they are wrong.

WB: I look good compared to him, don't I? [laughter]

ウォーレンはさりげなく示していますが、この会話に登場するもうひとつの大切なことは、個人的には「テコ」だと感じました。

2014年2月24日月曜日

トイレの中でも読んでいます(日本電産永守社長)

少し前の日経ヴェリタスを読んでいたところ、日本電産の永守社長へインタビューした記事がありました。その中で、買収候補等の企業を研究するために四季報や企業情報をよく読んでいる、と語っていました。今回ご紹介するのはその話題の一部で、当たり前のことながらも投資家として二重に参考になる発言です。引用元は、日経ヴェリタス第308号(2014/2/2-2/8)の記事「私の仕事術」からです。

この発言と似たようなことをチャーリー・マンガーも過去記事「株式を判断するのに使う指標(ウォーレン・バフェット)」で言っていました。

なお記事中の写真には、社内向けスローガンの書かれた漫画のポスター(スケート編)も写っていました。登場人物として永守社長自らが前面に出ているものの、レトロで誇張された画調が厳しい表現をうまく中和しているように感じられます。現代的なモーレツ日本企業らしさが出ており、なんとなしにジャック・ウェルチ時代のGEと対極にくる印象を受けました。

「風呂やトイレ、社用車の中にも置いて、いつでも読めるようにしています。各社の情報や数字はすべて頭の中に入っていますね。財務情報より、会社の弱点や強いところを把握することの方が重要なんです」。(p.56)

この発言と似たようなことをチャーリー・マンガーも過去記事「株式を判断するのに使う指標(ウォーレン・バフェット)」で言っていました。

なお記事中の写真には、社内向けスローガンの書かれた漫画のポスター(スケート編)も写っていました。登場人物として永守社長自らが前面に出ているものの、レトロで誇張された画調が厳しい表現をうまく中和しているように感じられます。現代的なモーレツ日本企業らしさが出ており、なんとなしにジャック・ウェルチ時代のGEと対極にくる印象を受けました。

2014年2月20日木曜日

相対取引価値による評価(セス・クラーマン)

ファンド・マネージャーのセス・クラーマンの著書『Margin of Safety』から、事業価値の話題がつづきます。今回は正味現在価値を求める手段のひとつ、相対取引価値についてです。前回分はこちらです。(日本語は拙訳)

相対(あいたい)取引価値

正味現在価値に関する評価方法のひとつとして相対取引価値がある。これは事業を値踏みする際に、世事に長けたやり手の実業家が同様のビジネスを最近購入した際に支払った評価倍率にもとづくやりかただ。相対取引価値は投資家が事業価値を評価する際の参考例として、過去の取引における経済性にもとづいた有用な経験則となりうる。しかし、この評価方法は必然的に弱点を伴っている。対象となる事業や業界において同じ企業はひとつもないが、相対取引価値ではそれらの違いを区別できないからだ。さらには、事業買収で支払われる倍率は時と共に変動するため、同様な案件が直近で生じてから評価基準が変化しているかもしれない。そして最後に、事業の買い手が常に適切で理にかなった価格を支払っているとはかぎらない。

相対取引価値が妥当かどうかは、その実業家がみずからの行動を理解しているという仮定にかかっている。言いかえれば、実業家が事業を買うときの金額が一貫して売上高や利益あるいはキャッシュ・フローの何倍かであれば、根底にある経済性について本質を突いた分析を実行した上での行動だと仮定できる。多分にそうしているものだ。結局は、高すぎる買収金額がつづけば損失を被ること必然となり、あとにつづく買い手たちは将来の案件において金額を抑えにかかる。反対に買収価格が低すぎると買い手は高いリターンを得られるので、それを知った者たちは価格を吊り上げ、超過利益が出ない水準まで達してしまう。そのような事態が生じるにせよ、長い期間でみると買収者の支払う金額は対象事業の根底にある経済性から離れることがある。

たとえば1980年代後半には、投資家が信頼していた「相対取引価値」は百戦錬磨の実業家が買収の際に支払う金額ではなくなった。ノンリコースのジャンク債[非遡及型の負債]を発行するという武器を手にした金融家が自前の資金をほとんど投じることなく、リスク対報酬をひどくゆがめ、また莫大な前払い手数料が得られるために、必要以上の金額を投じて企業買収に乗り出すようになった。実際に多くの場合において、投資家が相対取引価値を見積もる金額はジャンク債を発行する買い手の支払える金額となった。過剰な支払いによってそれらの買い手が破産しはじめることを、投資家は考慮しなくなってしまった。

根底にある事業の価値に対する倍率の歴史的水準を超えた金額が企業買収に使われるようになると、従来型の相対取引で買収する者は市場から締め出されてしまった。長い間、テレビ局には税引き前キャッシュ・フローの10倍ほどの値段が付けられていた。これが税引き前キャッシュ・フローの13倍から15倍へと値上がりした。消費者に対してフランチャイズを有するとみられている他の業界においても、多くの場合で同様に値段が高騰した。

1980年代半ばに、高騰した買収価格を信頼のおける相対取引価値だと誤って判断した投資家は、高すぎる株価やジャンク債に釣られてしまった。1989年や1990年になってノンリコースの融資がそれほど自由に受けられなくなると、評価倍率は歴史的水準あるいはそれ以下に回帰した。その結果、それらの投資家は大幅な損失を被ることとなった。

Private-Market Value

A valuation method related to net present value is private-market value, which values businesses based on the valuation multiples that sophisticated, prudent businesspeople have recently paid to purchase similar businesses. Private-market value can provide investors with useful rules of thumb based on the economics of past transactions to guide them in business valuation. This valuation method is not without its shortcomings, however. Within a given business or industry all companies are not the same, but private-market value fails to distinguish among them. Moreover, the multiples paid to acquire businesses vary over time; valuations may have changed since the most recent similar transaction. Finally, buyers of businesses do not necessarily pay reasonable, intelligent prices.

The validity of private-market value depends on the assumption that businesspeople know what they are doing. In other words, when businesspeople consistently pay a certain multiple of revenues, earnings, or cash flow for a business, it is assumed that they are doing so after having performed an insightful analysis of the economics. Often they have. After all, if the prices paid were routinely too high, the eventual losses incurred would inform subsequent buyers who would pay less in the future. If the prices paid were too low, the buyers would earn high returns; seeing this, others would eventually bid prices up to levels where excess profits could no longer be achieved. Nevertheless, the fact is that the prices paid by buyers of businesses can diverge from the underlying economics of those businesses for long stretches of time.

In the latter half of the 1980s, for example, the "private-market values" that investors came to rely on ceased to be the prices that sophisticated, prudent businesspeople would pay for businesses. Financiers armed with the proceeds of nonrecourse junk-bond offerings and using almost none of their own money were motivated by a tremendous skewing of their own risk and reward, as well as by enormous up-front fees, to overpay for corporate takeovers. Indeed, investors' assessment of private-market value in many cases became the price that a junk-bond-financed buyer might pay; investors failed to consider that those acquirers were starting to go bankrupt because the prices they had paid were excessive.

As the prices paid for businesses rose above historic multiples of underlying business value, traditional private-market buyers were shut out of the market. Television stations, which had been valued for many years at roughly ten times pretax cash flow, came to sell at prices as high as thirteen to fifteen times pretax cash flow. The prices of many other businesses with perceived consumer franchises became similarly inflated.

Investors who mistakenly equated inflated takeover prices with reliable private-market values were lured into overpaying for stocks and junk bonds in the mid-1980s. When nonrecourse financing became less freely available in 1989 and 1990, valuation multiples fell back to historic norms or below, causing these investors to experience substantial losses.

2013年12月4日水曜日

割引率の選択(セス・クラーマン)

ファンド・マネージャーのセス・クラーマンの著書『Margin of Safety』からご紹介します。前回からのつづきですが、今回と次回は「割引率」の話題になります。この話題は地味で見送ってしまいがちですが、遠くない将来に振り返りたくなる話題だと感じています。第8章「事業価値の算出という技」(The Art of Business Valuation)からの引用です。(日本語は拙訳)

割引率の選択

現在価値分析を構成するもうひとつの要素である割引率をどう設定するか、投資家が十分に考慮することはめったにない。投資家にとっての割引率とは事実上、現在と将来における金銭価値の差異を埋めるための金利である。将来よりも現在消費することを強く望んだり、不確実な将来よりも確実な現在に信頼をおく投資家は、投資先へ高い割引率を適用するだろう。一方で予測が的中するほうにかける投資家もいて、彼らは低い割引率を採用するだろう。その場合は将来のキャッシュフローに対して、現時点で保有しているのとほとんど差がない価値を与えることになる。

しかし、将来得られる一連のキャッシュフローに適用すべき唯一正しい割引率など存在しないし、それを選ぶための正確な方法もない。ある特定の投資に対する適切な割引率とは、投資家が将来よりも現在の消費をどれだけ重んじるかだけで決まるものではない。他の要因、つまり本人のリスクに対する考え方やその投資対象を検討したことで認識されたリスク、あるいは別の投資候補におけるリターン率にも左右される。

投資家は単純化しすぎる傾向がある。割引率を選定する方法はその典型と言えよう。検討対象の投資先が持つ性質にもかかわらず、万能の割引率として非常に多くの投資家が日常的に使っている値が10%だ。この数字はキリがよくて覚えやすく、そして使いやすいが、場合によってはよい選択だと言えないこともある。

適切な割引率を選ぶ際には、投資から得られる将来のキャッシュフローに関する潜在的なリスクを考慮しておかなければならない。無リスクの短期投資であれば(そのようなものが存在すればだが)、現在流通している財務省短期証券の利率で割り引く必要がある。先にふれたように、この証券は無リスク金利を代用するものとみなされている。対照的に、低級の債券が市場で取引される際には、12%から15%あるいはそれ以上の利率で割り引かれている。これは、キャッシュフローが約束通りに支払われるのか投資家が疑問視していることを反映している。

投資家が将来のキャッシュフローを予測する際には、割引率を保守的に選ぶことは不可欠である。キャッシュフローの時期や規模に左右されるため、割引率が少し変動しただけでも現在価値の計算にかなりの影響を与えかねないからだ。

事業価値は、割引率の変化やそれ以前に金利変動によっても影響される。利率すなわち割引率が固定されていれば、投資価値を決定するのは容易だろう。しかし投資家はそれらが変動する事実を受け入れた上で、金利変動からくるポートフォリオへの影響を抑制できるような対策を講じなければならない。(p.125)

The Choice of a Discount Rate

The other component of present-value analysis, choosing a discount rate, is rarely given sufficient consideration by investors. A discount rate is, in effect, the rate of interest that would make an investor indifferent between present and future dollars. Investors with a strong preference for present over future consumption or with a preference for the certainty of the present to the uncertainty of the future would use a high rate for discounting their investments. Other investors may be more willing to take a chance on forecasts holding true; they would apply a low discount rate, one that makes future cash flows nearly as valuable as today's.

There is no single correct discount rate for a set of future cash flows and no precise way to choose one. The appropriate discount rate for a particular investment depends not only on an investor's preference for present over future consumption but also on his or her own risk profile, on the perceived risk of the investment under consideration, and on the returns available from alternative investments.

Investors tend to oversimplify; the way they choose a discount rate is a good example of this. A great many investors routinely use 10 percent as an all-purpose discount rate regardless of the nature of the investment under consideration. Ten percent is a nice round number, easy to remember and apply, but it is not always a good choice.

The underlying risk of an investment's future cash flows must be considered in choosing the appropriate discount rate for that investment. A short-term, risk-free investment (if one exists) should be discounted at the yield available on short-term U.S. Treasury securities, which, as stated earlier, are considered a proxy for the risk-free interest rate. Low-grade bonds, by contrast, are discounted by the market at rates of 12 to 15 percent or more, reflecting investors' uncertainty that the contractual cash flows will be paid.

It is essential that investors choose discount rates as conservatively as they forecast future cash flows. Depending on the timing and magnitude of the cash flows, even modest differences in the discount rate can have a considerable impact on the present-value calculation.

Business value is influenced by changes in discount rates and therefore by fluctuations in interest rates. While it would be easier to determine the value of investments if interest rates and thus discount rates were constant, investors must accept the fact that they do fluctuate and take what action they can to minimize the effect of interest rate fluctuations on their portfolios.

2013年11月30日土曜日

リスキーだがバブルではない(ハワード・マークス)

Oaktreeの会長ハワード・マークスが久しぶりに新しいメモを公開していました。市場全体の動向を描写し、まとめとして現在の価格水準に触れています。そのまとめの部分を引用します。(日本語は拙訳)

The Race Is On (Oaktree) (PDFファイル)

ハワード・マークスが「まだだ」と言っており、またマクロの状況はあまり気にすべきではないのですが、個人的には中国の過剰な外貨借入れの現状を警戒しています(参考記事)。

The Race Is On (Oaktree) (PDFファイル)

リスクを許容する風潮は最近になってあきらかに高まっています。リスク資産から得られる高いリターンによって相変わらず助長され、市場はさらに過熱しています。セクターによって利益の幅はありますが、2008年末の金融危機や2009年初の株式市場の危機のどん底以来、市場はもっともリスキーな状況にあると断言できます。そしてさらに危険は増しています。

「売り」の合図なのか、それとも別のものか

しかし私は、今が市場から退出する時期だとは考えていません。価格や評価水準は数年前より高くなり、危険な行動も見受けられます。しかし肝心なのはその度合いで、危険な領域にはまだ達していないとみています。

第一の理由として、すでに述べたようにリスクの絶対量が2006-07年ほどには大きくないことがあります。この現代では、金融面での奇跡がたびたび(高頻度とも称される)は起きませんし、借入に依存する水準もそれほどではありません。

第二に、価格や評価水準が高すぎるほどには進展していないことです(S&P500のPERは16前後ですが、これは戦後平均の水準です。一方、2000年には30台前半つまり行き過ぎでした)。

リスクを許容する風潮が高まれば、それに注意を払いながら自分のことに集中すべきです。しかし強く危険視すべきなのは、評価水準が大きく上昇したときです。まだその状況ではないと私は考えます。ほとんどの資産クラスが満額まで値付けされており、多くの場合妥当な水準の上位に達していますが、しかしバブル型の高値にはなっていません。(後略)

Certainly risk tolerance has been increasing of late; high returns on risky assets have encouraged more of the same; and the markets are becoming more heated. The bottom line varies from sector to sector, but I have no doubt that markets are riskier than at any other time since the depths of the crisis in late 2008 (for credit) or early 2009 (for equities), and they are becoming more so.

Is This a Sell Signal? If Not, Then What?

No, I don't think it's time to bail out of the markets. Prices and valuation parameters are higher than they were a few years ago, and riskier behavior is observed. But what matters is the degree, and I don't think it has reached the danger zone yet.

First, as mentioned above, the absolute quantum of risk doesn't seem as high as in 2006-07. The modern miracles of finance aren't seen as often (or touted as highly), and the use of leverage isn't as high.

Second, prices and valuations aren't highly extended (the p/e ratio on the S&P 500 is around 16, the post-war average, while in 2000 it was in the low 30s: now that's extended).

A rise in risk tolerance is something that should get your attention and focus your concentration. But for it to be highly worrisome, it has to be accompanied by extended valuations. I don't think we're there yet. I think most asset classes are priced fully - in many cases on the high side of fair - but not at bubble-type highs.

ハワード・マークスが「まだだ」と言っており、またマクロの状況はあまり気にすべきではないのですが、個人的には中国の過剰な外貨借入れの現状を警戒しています(参考記事)。

2013年11月18日月曜日

ヤクトマン・ファンドの投資方針

少し前の投稿で引用した文章に、ファンド・マネージャーのドナルド・ヤクトマンが短期的な成績を追わず、現金比率を上げている旨の一節がありました(過去記事)。彼の今年の成績を確認してみると、年初来の成績はS&P500を若干下回っています。また昨年2012年も5%ほど差をつけられていました(ファンドの成績資料PDFファイル)。もちろん現在の彼の動きは長期的な観点によるものであり、はたからそれを観察できるのは個人的には勉強になります。

今回引用するのは、ヤクトマン・ファンドのWebサイトに掲載されているファンドの紹介文です。ウォーレン・バフェットの説明する内容とよく似ていますが(過去記事など)、もう少し具体的な表現に踏み込んだものもあります。(日本語は拙訳)

Managers Investment Group: Yacktman Fund - Overview

(追記2013/11/19) 「ウォーレン・バフェットの説明する内容とよく似ている」と書きましたが、通りがかりさんからコメントでご指摘頂いたように、「似ている点はあるが、ちがいもある」といった表現のほうが適切でした。

今回引用するのは、ヤクトマン・ファンドのWebサイトに掲載されているファンドの紹介文です。ウォーレン・バフェットの説明する内容とよく似ていますが(過去記事など)、もう少し具体的な表現に踏み込んだものもあります。(日本語は拙訳)

Managers Investment Group: Yacktman Fund - Overview

<ファンドの狙い>

ヤクトマン・ファンドが主眼とするのは、長期でみたときの資産形成です。そのうえで、現在における収入も副次的な目標としています。当ファンドでは主に米国企業の普通株に投資しますが、多くの銘柄には分散させません。対象企業の規模は問いません。配当金の支払い状況は考慮しますが、必ずしも必須ではありません。[当ファンド]ヤクトマンは規律に基づいた投資戦略に従い、割安と考えられる価格で成長企業を購入します。この方針こそ、「成長株投資」と「バリュー株投資」の最良の特徴を合わせたものとヤクトマンは信じております。株式を購入する際には、次の3つの属性のうち1つ以上を有していると確信できる企業を追求します。その属性とは、第一に優れたビジネスであること、第二に株主本位の経営がされていること、第三が安値で購入できることです。

<優れたビジネスについて>

優れたビジネスは、以下の項目の1つ以上が該当することがあります。

・主力の製品群あるいはサービス群のマーケットシェアが高いこと。

・対有形資産比でのキャッシュ・リターン率が高いこと。

・相対的に少ない設備投資で、成長し続けながらもキャッシュを創出できること。

・顧客の購買頻度が高く、製品ライフサイクルが長いこと。

・独自のフランチャイズを有していること。

<株主本位の経営について>

株主本位の経営者であれば、過大な報酬をみずからに支払うことなく、会社が稼いだ金の使途を賢明に決めるものとヤクトマンは信じています。ヤクトマンが追い求めるのは次のような企業です。

・事業に再投資し、かつ余剰資金をうみだせる企業

・相乗効果のある買収をおこなう企業

・自己株式を買い戻す企業

<安い購入価格について>

ヤクトマンがさがす株式とは、投資家が企業全体を買う際に支払ってもよいと考える金額よりも安く売られているものです。

個々の企業の株価は短期間で大きく変動することがあります。そのような価格変動は企業の本質的な業績の変化と必ずしも連動するわけではありません。よってヤクトマンは通常、購入すべき機会を好んで待つことにしています。そのような機会は市場全体の価格動向と関係なしに出現することがあります。

Fund Focus

The Yacktman Focused Fund seeks long-term capital appreciation, and, to a lesser extent, current income. The Fund is non-diversified and mainly invests in common stocks of United States companies of any size, some, but not all of which, pay dividends. Yacktman employs a disciplined investment strategy, buying growth companies at what it believes to be low prices. Yacktman believes this approach combines the best features of "growth" and "value" investing. When they purchase stocks they generally search for companies they believe to possess one or more of the following three attributes: (1) good business; (2) shareholder-oriented management; or (3) low purchase price.

Good Business

A good business may contain one or more of the following:

High market share in principal product and/or service lines;

A high cash return on tangible assets;

Relatively low capital requirements allowing a business to generate cash while growing;

Short customer repurchase cycles and long product cycles; and

Unique franchise characteristics.

Shareholder-Oriented Management

Yacktman believes a shareholder-oriented management does not overcompensate itself and wisely allocates the cash the company generates. Yacktman looks for companies that:

Reinvest in the business and still have excess cash;

Make synergistic acquisitions; and

Buy back stock.

Low Purchase Price

Yacktman looks for a stock that sells for less than what an investor would pay to buy the whole company.

The stock prices of individual companies can vary significantly over short periods of time, and such price movements are not always correlated with changes in company fundamental performance. Accordingly, Yacktman generally prefers to wait for buying opportunities. Such opportunities do not always occur in correlation with overall market performance trends.

(追記2013/11/19) 「ウォーレン・バフェットの説明する内容とよく似ている」と書きましたが、通りがかりさんからコメントでご指摘頂いたように、「似ている点はあるが、ちがいもある」といった表現のほうが適切でした。

2013年10月14日月曜日

日本株投資での反省(モーニッシュ・パブライ)

モーニッシュ・パブライが自分のファンドの年次総会で発言した内容がGuruFocusに投稿されていました。興味をひく話題がいくつかありましたので、ご紹介します。(日本語は拙訳)

2013 Pabrai Investment Funds Annual Meeting Notes - Chicago (GuruFocus)

なお、文中で登場する「ネット・ネット」とは、バリュー投資の世界では一般的な評価基準です。たとえばこちらのサイトに定義が記述されています。

この話題は何度か取り上げてきましたが、過去記事「現金豊富な日本株の問題なところ(FPA)」できれいに断罪されています。

次は米アップル社の話題です。

最後の話題は、株式売却の基準と価値評価時に使う割引率についてです。

2013 Pabrai Investment Funds Annual Meeting Notes - Chicago (GuruFocus)

なお、文中で登場する「ネット・ネット」とは、バリュー投資の世界では一般的な評価基準です。たとえばこちらのサイトに定義が記述されています。

パブライのファンドは2010年10月から日本株のネット・ネット銘柄に束で投資していたが、全ポジションを売却した。利益は配当込みで2.2%、年率換算で1.4%だった。2010年10月以降でみると日本の株式市場は大幅に上昇しており、これは意外な数字だ。説明しようとするモーニッシュは言葉をさがして、ベン・グレアムの『証券分析(1940年版)』からいくつか引用した。そのひとつが次のとおり。

しかしながら、そのような割安銘柄に投資する際には、その時の市場動向をいくぶん考慮にいれる必要がある、と言えるかもしれない。かなり奇妙なことだが、この種類の運用は価格水準が極端に高くもなく安くもない時期において、相対的に最上の成果をあげている。

パブライは話を広げ、市場が底をつけているときにはネット・ネット銘柄に目をつけるよりも、市場と共に急激に下落している質の高い企業を買うのがいいと述べた。市場全体が上昇すると、投資家は質の高い企業や話題になっている銘柄へと注目を移し、ネット・ネットはまたもや無視されるからだ。

投資先には日比谷総合設備(1982)や菱洋エレクトロ(8068)が含まれており、どちらもNCAV[正味流動資産; Net Current Asset Value]以下で取引されていた。投資した頃には、キャッシュフローは黒字かつ一貫したもので、利益も計上していた。また両社とも経営陣は自社株を買い戻していた。日比谷への投資では利益が若干出たが、菱洋は15%の損失におわった。

(中略)

ひきつづき日本のネット・ネット銘柄について、なぜ全ポジションを処分したのかという質問。トレンドが形成中の市場環境では、ネット・ネット戦略が働かないのはベン・グレアムの主張するとおりではないのか。

パブライが答えるに、余裕資金をもっておきたかったが、当時は納得できるほどの現金比率ではなかったので、一連のネット・ネット銘柄を売却した、とのことだった。また、日本企業の経営陣は会社の価値を株主へ還元する意思や能力に欠けている、と市場が否定的にとらえている様子にも彼は言及した。

The Pabrai funds invested in a basket of Japanese net-nets starting October 2010. Pabrai has exited all the positions with a realized gain of 2.2% including dividends, or 1.4% annualized. To me, this is surprising as the Japanese market has advanced significantly since October 2010. In search of explanation, Mornish referred to a few quotes from Ben Graham from the 1940 edition of "Security Analysis." Here is one:

"It may be pointed out, however, that investment in such bargain issues needs to be carried on with some regard to general market conditions at the time. Strangely enough, this is a type of operation that fares best, relatively speaking, when price levels are neither extremely high nor extremely low."

Pabrai expanded on this by stating that when the market bottoms it's much better to buy quality companies that have fallen precipitously with the market than focus on net-nets. When the market flies, net-nets are also ignored because investors shift their focus to both quality companies and story stocks.

Examples include Hibiya Engineering (TSE:1982) and Ryoyo Electro (TSE:8068). Both were trading below NCAV at the time of his investment, generating profits as well as positive and consistent cash flows. Managements of both companies were also repurchasing shares. Hibiya ended up just a little bit profitable, and Ryoyo turned out be a 15% loss.

(snip)

1. Further comments on the Japanese net-net investments. Why did the funds exit all net-net positions? Is Ben Graham right about the net-net strategy not working in a trending market?

Pabrai said he wanted to have the optional of cash, and he wasn't comfortable with the level of cash holdings. Therefore, he exited the net-net basket. He also mentioned that the market is skeptical about Japanese companies' managements' willingness and ability to unlock value for shareholders.

この話題は何度か取り上げてきましたが、過去記事「現金豊富な日本株の問題なところ(FPA)」できれいに断罪されています。

次は米アップル社の話題です。

<質問者> 昨年の今頃はアップル(AAPL)の株価は連日上昇し、700ドルをつけました。昨年のある会合で、アップルは買わないのかと質問されていましたね。なぜ買わないのですか。

<パブライ> アップルは、非常にすばらしいフランチャイズを有した特上の企業です。そのアップルに近づかない理由のひとつは、急速に変化する業界だからです。さらにもうひとつ待ったをかけるのが、アップルは超大型株だからです。大型優良株で2倍や3倍になるものは見つからないものです。一方、もっと小型の銘柄であればよい機会がみつけられます。

17. At this time last year, Apple (AAPL) was going up everyday up to around $700, and someone during the meeting last year asked you if you would buy Apple. Why did you not buy Apple?

Apple is a fantastic business with an incredible franchise. What keeps him away from Apple is because it is in an industry with rapid changes. The second thing that dissuades him: Apple is a super large cap and you are not going to find 2x, 3x returns in large cap blue chips. You will find better opportunities in smaller caps.

最後の話題は、株式売却の基準と価値評価時に使う割引率についてです。

<質問者> 売却についてどのようにお考えですか。また金利変動は、お使いになっている割引率に影響しますか。

<パブライ> ふつうは、本源的価値の90%の時点で売却しています。また金利の件ですが、適用している割引率には影響しません。概して6%から9%であればよいと考えています。

24. What are your thoughts on selling? Does the rise or fall of interest rates change the discount rate you use?

Typically he sells at 90% of intrinsic value. The interest rate doesn't really affect the discount rate he uses. In general, a discount rate of 6% to 9% should be okay.

2013年10月6日日曜日

事業価値の評価について(セス・クラーマン)

ファンド・マネージャーのセス・クラーマンの著書『Margin of Safety』から、ひきつづき事業価値の話題をご紹介します。第8章「事業価値の算出という技」(The Art of Business Valuation)からの引用です。前回分はこちらです。(日本語は拙訳)

事業価値の評価

バリュー投資家であるからには、内在価値よりも割安な水準で買わなければならない。そこで、投資の検討対象が潜在的な超過価値(バリュー)を有しているか分析する際には、事業価値を評価することから始める。

事業価値を評価する方法には非常に多くのやりかたがあるが、私が有用だと思えるものは3種類しかない。ひとつめが「継続価値」を分析する方法で、正味現在価値(NPV)分析として知られている。NPVは、事業がうみだすと期待される将来のキャッシュフローを割り引くことで算出される価値である。その際に、継続価値をもとめる近道として「相対(あいたい)取引価値」を評価する方法がよく使われているが、これには欠陥もある。この近道を使う投資家は、世事に長けた実業家が事業に対して支払ってもよいと考える金額で評価する。事実上、この近道で事業を評価する際には、過去にあった比較可能な買収案件での取引価格を何倍かして算出している。

2番目の事業価値評価分析の方法は、「清算価値」分析である。これは、会社を廃業して資産を売却することで得られる収益の期待値を算出する。この方法の変種のひとつとして、「解散価値」を分析するやりかたがある。これは、ある企業を部分に切り分けてそれぞれを最高値で評価して算出する。その際に、各部分が事業を継続するか否かは問わない。

価値評価の3つ目の方法は「市場価値」分析で、企業全体あるいは本体から切り離して捉えることのできる子会社について、株式市場で取引された場合の価格を評価する。この方法は他の2つとくらべて信頼性が低く、価値をはかる一基準として役に立つこともある、といったものにすぎない。

これらの価値分析手法にはそれぞれ長短があり、常に正確な価値をもたらすものはない。残念ながらこれ以上の価値分析方法がないので、それらから算出される価値を検討せざるをえない。その際に各評価の結果がかなり離れていれば、投資家としては安全なほうへ逸脱すべきだ。

Business Valuation

To be a value investor, you must buy at a discount from underlying value. Analyzing each potential value investment opportunity therefore begins with an assessment of business value.

While a great many methods of business valuation exist, there are only three that I find useful. The first is an analysis of going-concern value, known as net present value (NPV) analysis. NPV is the discounted value of all future cash flows that a business is expected to generate. A frequently used but flawed shortcut method of valuing a going concern is known as private-market value. This is an investor's assessment of the price that a sophisticated businessperson would be willing to pay for a business. Investors using this shortcut, in effect, value businesses using the multiples paid when comparable businesses were previously bought and sold in their entirety.

The second method of business valuation analyzes liquidation value, the expected proceeds if a company were to be dismantled and the assets sold off. Breakup value, one variant of liquidation analysis, considers each of the components of a business at its highest valuation, whether as part of a going concern or not.

The third method of valuation, stock market value, is an estimate of the price at which a company, or its subsidiaries considered separately, would trade in the stock market. Less reliable than the other two, this method is only occasionally useful as a yardstick of value.

Each of these methods of valuation has strengths and weaknesses. None of them provides accurate values all the time. Unfortunately no better methods of valuation exist. Investors have no choice but to consider the values generated by each of them; when they appreciably diverge, investors should generally err on the side of conservatism.

2013年9月18日水曜日

価値のとりうる範囲(セス・クラーマン)

ファンド・マネージャーのセス・クラーマンの著書『Margin of Safety』をご紹介しています。前回につづいて第8章「事業価値の算出という技」(The Art of Business Valuation)から引用します。(日本語は拙訳)

価値のとりうる範囲

負債性の証券とは異なり、事業からは契約によって定められるキャッシュフローが得られない。そのため、債券のようには価値を正確に値踏みすることができない。企業ひいてはその部分的な所有権を意味する株式の価値を一点読みするのがむずかしいことを、ベンジャミン・グレアムは理解していた。彼とデイヴィッド・ドッドは著書『証券分析』で、「価値のとりうる範囲」という概念について次のように話題を展開している。

根本的なこととしてあげておきたいのは、証券分析とは対象とする証券の本源的価値を正確に見極めるものではないことだ。価値が適正であることを証明できればよい。たとえば債券の安全性を保証したり、株式を購入する理由を正当化したり、あるいは市場価格とくらべて価値が十分に大きいか、反対に十分に小さいかを示せばよい。そのような目的を達成するには、本源的価値がだいたい概算でわかれば十分と思われる。

実際にグレアムは、「1株当たり正味運転資本」と呼ばれる値を計算することが多かった。これは企業の清算価値を概算で見積ったものだ。このおおまかな近似を使ったことで、企業の価値をそれ以上正確には追究できなかったことを、彼は語らずとも認めている。実は投資家にとって、事業価値を正確に算出するのがむずかしいことは容易に説明できる。企業が売りに出された時にウォール街はたいてい評価額を示すが、これが広い幅にわたることを考えればよいのだ。たとえば1989年には、カンポー社がブルーミングデールズ[デパート]を売り出すことになり、買収を希望する先がないか打診した。またハーコート・ブレース・ジョバノビッチ社は、子会社のシー・ワールドを競売に出した。ヒルトン・ホテルは身売りすることになった。どの案件でもウォール街が出した企業価値の評価額は広い幅にわたっており、最高額は最低額の2倍になった。大量の情報を手にした熟練分析家であっても、注目の集まる評判の高い企業の価値をこれ以上に確信をもって評価できないのだとしたら、限られた公開情報しか入手できない投資家が自分ならばもっと正確にできると盲信すべきではない。

市場というものは、投資家が異なった意見を持っているおかげで存在している。もし証券の価値が正確に判断できるのであれば、見解の相違はずっと小さくなる。そして市場価格があまり変動しなくなり、取引自体も縮小する。ファンダメンタル志向の投資家が買い手にまわるときは購入金額よりも証券の価値が大きくなければならず、売り手のときは売却金額よりも価値のほうが小さくなければならない。そうでないと、取引が生じない。価値を認識する際に、将来に対する仮定が異なっていたり、資産を使うねらいが異なっていたり、異なった割引率を適用することで、買い手と売り手の見解に相違が生じるようになる。売買されるあらゆる資産は、価値の面で幅を持っている。その範囲は買い手による価値から売り手による価値までで、実際に取引される価格はその間のどこかに決まる。

たとえば1991年のはじめには、トンカ社のジャンク債には額面価額よりも大幅に割り引かれた値がついていた。また株式1株の価格は数ドルだった。同社は投資銀行やハズブロ社から売却を打診されたが、あきらかにハズブロは他の買い手よりも多額を支払うつもりだった。なぜなら、2社を合わせることで実現できる経済性を考慮していたからだ。実際のところトンカがハズブロに対して供給したキャッシュフローは、単体当時あるいは他のほとんどの買い手に対するものと比較して、かなり多額なものとなった。トンカの価値に対して、金融市場とハズブロの両者の見解は、鮮やかなまでに異なっていた。その相違は、ハズブロによる買収という形で幕引きとなった。

A Range of Value

Businesses, unlike debt instruments, do not have contractual cash flows. As a result, they cannot be as precisely valued as bonds. Benjamin Graham knew how hard it is to pinpoint the value of businesses and thus of equity securities that represent fractional ownership of those businesses. In Security Analysis he and David Dodd discussed the concept of a range of value:

The essential point is that security analysis does not seek to determine exactly what is the intrinsic value of a given security. It needs only to establish that the value is adequate - e.g., to protect a bond or to justify a stock purchase - or else that the value is considerably higher or considerably lower than the market price. For such purposes an indefinite and approximate measure of the intrinsic value may be sufficient.

Indeed, Graham frequently performed a calculation known as net working capital per share, a back-of-the-envelope estimate of a company's liquidation value. His use of this rough approximation was a tacit admission that he was often unable to ascertain a company's value more precisely.

To illustrate the difficulty of accurate business valuation, investors need only consider the wide range of Wall Street estimates that typically are offered whenever a company is put up for sale. In 1989, for example, Campeau Corporation marketed Bloomingdales to prospective buyers; Harcourt Brace Jovanovich, Inc., held an auction of its Sea World subsidiary; and Hilton Hotels, Inc., offered itself for sale. In each case Wall Street's value estimates ranged widely, with the highest estimate as much as twice the lowest figure. If expert analysts with extensive information cannot gauge the value of high-profile, well-regarded businesses with more certainty than this, investors should not fool themselves into believing they are capable of greater precision when buying marketable securities based only on limited, publicly available information.

Markets exist because of differences of opinion among investors. If securities could be valued precisely, there would be many fewer differences of opinion; market prices would fluctuate less frequently, and trading activity would diminish. To fundamentally oriented investors, the value of a security to the buyer must be greater than the price paid, and the value to the seller must be less, or no transaction would take place. The discrepancy between the buyer's and the seller's perceptions of value can result from such factors as differences in assumptions regarding the future, different intended uses for the asset, and differences in the discount rates applied. Every asset being bought and sold thus has a possible range of values bounded by the value to the buyer and the value to the seller; the actual transaction price will be somewhere in between.

In early 1991, for example, the junk bonds of Tonka Corporation sold at steep discounts to par value, and the stock sold for a few dollars per share. The company was offered for sale by its investment bankers, and Hasbro, Inc., was evidently willing to pay more for Tonka than any other buyer because of economies that could be achieved in combining the two operations. Tonka, in effect, provided appreciably higher cash flows to Hasbro than it would have generated either as a stand-alone business or to most other buyers. There was a sharp difference of opinion between the financial markets and Hasbro regarding the value of Tonka, a disagreement that was resolved with Hasbro's acquisition of the company.

2013年9月10日火曜日

投資というプロセスにおける決定的な点(ウォーレン・バフェット)

ウォーレン・バフェットが1994年にネブラスカ大学でおこなった講演その7です。前回と同じように有名な話題がつづきますが、講演全体の文脈の一部としてとらえれば、また違う印象でうけとめられるかと思います。(日本語は拙訳)

本ブログを始めて3年目に入りました。いつもお読みになってくださる方にはお礼申し上げます。これからもよろしくお願い致します。

<質問者> 将来を占うとしたら、これから数年間はどのセクターの株に着目していきますか。どういった種類の株が流行ると思いますか。

<ウォーレン> ずいぶん学術的な質問ですね。少しばかり仮想的なところがありますね。

<質問者> 1日をどのように過ごされているのですか。

<ウォーレン> 核心をついてきますね。そうですね、文章を読むのに大量の時間をあてています。最低でも6時間ですが、まあそれ以上でしょう。そのほかに、1,2時間は電話で話します。あとは考えています。そんなところでしょうか。バークシャーには会議というものがありません。したことがないのです。全国にビジネスを展開しているので従業員は約2万名になっていますが、[子会社の]マネージャーとの会議に出たのはこの20数年で一度だけです。健康保険の話題をしたきりです。ですが、彼らがオマハに来たことはありません。プレゼンもしないのでプロジェクターなどは一切不要です。取締役会は1年間に一度、年次株主総会の直後にやります。昼食をとりながらで、それでおわりです。ずばり言いますと、会議がきらいなのです。これまで自分が楽しめるようなものごとを築いてきました。たくさん読むのが好きですし、いろいろ考えることもそうです。自分でビジネスを大きくしたり、ビジネスを始めるのでしたら、自分が楽しめないものを築き上げるのは、わたしからすればなにかおかしい感じがします。絵を描くのと同じです。完成したときに作品をながめて、よろこびを感じるような絵を描くべきですね。

さて、この午後に何を買うべきかという最初の質問にはお答えしませんでした。というのは、どうすればいいのかよくわからないからです。株式市場がどうなるのか、ある銘柄の株価が近いうちにどうなるかは、わたしにはまったくわかりません。わたしたちは、株式を事業の一部分とみなして保有するようにしています。これは、投資というプロセスにおける決定的な点だと考えています。株式のことをただの銘柄コードと考えたり、単に値段が上がったり下がったりするものなどと考えず、自分が所有する事業だと考えるようにしてください。[ネブラスカ大学のある街]リンカーンでビジネスを買う決断をするかのように考えるのです。クリーニング店や食料雑貨をあつかう小売店などを買おうとなれば、買った事業を明日売ろうかとか来週売ろうかなどとは、ふつうは考えないものです。そうではなく、長期的にみて良い事業なのかどうか検討するでしょう。それがわたしたちが実践していることです。ですからバークシャーのポートフォリオには、わたしたちが所有したいと願うたぐいの事業がならんでいるのがご覧いただけるかと思います。

最大の保有銘柄はコカ・コーラですが、ジレットにも大きく投資しています。その2社は、それぞれの業界でもっとも支配的な位置にある企業です。また変化が激しくない企業でもあります。その世界が急速に変化するようなものには投資したいとは考えていません。変化をうまく見極めたり、こちらの先生よりもうまくやれるとは思えないからです。ですから本当に買いたいと思っているのは、すごく安定していて非常に良好な経済性を有していけるものです。コカ・コーラ社は全世界の清涼飲料水の47%を販売しています。世界中で1日に飲まれる量は、1杯8オンス[=約250ml]換算で7億5,000万杯になります。もし製品の値段を1ペニー[=0.01ドル]値上げできれば、税引前利益が25億ドル増えることになります。わたしが理解できるのはこういうことです。またジレットですが、この会社もすばらしいです。世界中のひげそり用かみそりの替え刃を、ドル換算にして60%以上供給しています。夜になって寝床に入ると、こう考えます。わたしが寝ている間に何十億人という男性の顔にだまっていてもひげが伸びてくるのだなと。それこそ、ぐっすり眠りにつけるわけです。

Q. If you could look in your crystal ball, what kind of sector stocks would you look into in the next few years? What kind of stocks do you think will boom?

A. That's an academic question if I ever heard one. Just a little theoretical.

Q. What exactly do you do all day?

A. Getting right to the core here, aren't you? I spend an inordinate amount of time reading. I probably read at least six hours a day, maybe more. And I spend an hour or two on the telephone. And I think. That's about it. We have no meetings at Berkshire. We've never had. We have businesses around the country; we have some 20,000 employees, but we've only had one meeting of our managers in the twenty-some years I've been there, to talk about health care - one time. But, they never come to Omaha. We never have presentations. We don't have a slide projector. We don't do any of that sort of thing. Our board of directors meets once a year, right after the annual meeting. We have lunch and that's it, because I hate meetings, frankly. I have created something that I enjoy: I happen to enjoy reading a lot, and I happen to enjoy thinking about things. It is a little crazy, it seems to me, it you are building a business and creating a business, not to create something you are going to enjoy when you get through. It's like painting a painting. I mean, you ought to paint something you are going to enjoy looking at when you get through.

Now, I know I'm avoiding your first question about what I should buy this afternoon. I don't think much about that. I don't think at all about what the stack market will do or what given stocks will do in the very short term. We do try to own, and to look at stocks, as pieces of businesses. And, that is crucial in my view to the investing process; that is, to not think about a stock as a little ticker symbol or something that goes up or down, or something of the sort, but to think about the business that you own.... Some way if you were deciding on a business to buy in Lincoln. You might think about buying a dry cleaning store or a grocery store or whatever. You wouldn't think about what this business is going to be selling for tomorrow or next week or anything. You would think about whether it's going be a good business over a long period of time. And that's what we try and do. So, if you look at the portfolio of Berkshire, you will see the kind of businesses that we like to own.

Our biggest single holding is Coca-Cola. We own a lot of Gillette. Those are two of the most dominant companies in the world in their field, And they are also companies that are not subject to a lot of change. We don't want to own things where the world is going to change rapidly because I don't think I can see change that well or any better than the next fellow. So, I really want something that I think is going to be quite stable, that has very good economics going for it. Coca-Cola sells 47% at all the soft drinks in the world. That is seven hundred and fifty million eight-ounce servings a day around the world. That means if you increase the price of Coke one penny, you would add two and a half billion dollars pre-tax to the earnings. So, that's the kind of thing I can figure out. And, Gillette, I mean Gillette is marvelous. Gillette supplies over 60% of the dollar value of razor blades in the world. When I go to bed at night and think of all those billions of males sitting there with hair growing on their faces while I sleep, that can put you to sleep very comfortably.

本ブログを始めて3年目に入りました。いつもお読みになってくださる方にはお礼申し上げます。これからもよろしくお願い致します。

2013年6月8日土曜日

株式を判断するのに使う指標(ウォーレン・バフェット)

2013年5月開催のバークシャー・ハサウェイ年次株主総会のトランスクリプトから引用します。前回分はこちらです。(日本語は拙訳)

蛇足になりますが、ある石油会社が気になったことをきっかけに、石油業界を勉強しつづけています。今回引用したチャーリーの指摘は耳が痛いです。

蛇足その2です。昨日7日(金)は手持ちの日本株がそれなりの水準まで下落したため、わずかな金額ですが、売却してきた株を買い戻したり、買い増しをしました。割安と判断した指標はPERとPBRです。チャーリーの教えにことごとく背いているようで、微妙な思いがあります。

<質問37:シアトル在住の株主> 株式を判断するのに、どのような定量的指標を使っていますか。

<ウォーレン・バフェット> われわれは株式という切り口ではなく、つねにビジネスを買うという観点でみています。バスケットボールのコーチなら身長が7フィート[≒213cm]以上の選手をさがすように、事業に応じてちがう数字で判断しています。ただしわれわれには深く考察できないものもありますし、わからないことがあるのも承知しています。ときには、それによって考え直すこともあります。バンク・オブ・アメリカの件では、風呂に入っていたこと自体は重要ではありませんでした[案件をひらめいたときの場所]。同行について書かれた本"Biography of a Bank"を50年ほど前に読んだのですが、すばらしい内容でしたよ。保険業界をみるときとイスカル[買収した切削工具メーカー]とでは違った観点で考えますし、ブランドがものをいう業界となれば、また別の見方になります。コークのようにうまくいくブランドもあれば、そうでないものもありますね。風呂に浸かっているときにバンカメはいい投資かもしれないと思いあたり、電話をかけたのです。そのときは、PERやPBRを厳密に計算したわけではありません。会社が5年後にどうなっているかを考え、価格と現在価値がかい離していると思ったのです。

<チャーリー・マンガー> 何かの指標にもとづいて株を買うやり方はよくわかりませんね。知りたいのは、ある企業が実のところどのように機能しているかです。ウォーレンはコンピュータを使ってスクリーニングしていますか。

<ウォーレン> いいえ、どうやるのか知らないのですよ。ただしスクリーニングは使っていませんが、別の意味であらゆるものをふるいにかけています。だれかが提示してくれたかのように、あらゆるものについて考えるようにしているわけです。5年,10年後にどうなっているか、どこまでそれを確信できるか、そして価格にどれだけ織りこまれているか、ということをです。われわれでは答えがだせなかったり、未来がうまく見通せないと感じるビジネスも数多くあります。自動車業界をみてきて50年になりますが、あれは非常におもしろいビジネスですね。

<チャーリー> 10年後のBNSF[買収した鉄道会社]は競争優位を手にしているでしょうが、アップルや石油会社がどうなるかは我々には判断できないですね。

数学の得意な人は、数字を追いかけることで答えを見つけられると考えがちです。やるべきことは競争する上での企業の立ち位置を理解することで、そんなに簡単ではないですよ。必要なのはビジネスを知ることで、数学ではありません。

<ウォーレン> ベン・グレアムから教わったやりかたとはちがいますね。数字だけをみることになっていたら資金をうまく運用できていたか、なんともいえません。

<チャーリー> きっとお粗末な結果だったでしょうな(笑)。

Q37, Station 1: Seattle. Which quantitative metrics to judge a stock?

WB: We aren't looking at the aspects of stocks, but always are buying a business. If you were a basketball coach, you can look for all seven-footers. We look at different numbers for different businesses. We see certain things that shut out to us to look further. We also know what we can't know. Often we have a fact that slips back in which causes us to change our mind. The bathtub wasn't the central factor for Bank of America. I read a book 50 years ago, Biography of a Bank, a great book. We have certain things we look for in insurance. We have things that we think about which is different when we think about Iscar. There are things we think about when dependent on brands. Some brands travel well, like Coke, some don't. In the bath, I thought Bank of America might be good idea, so I gave him a call. It is not because I calculated some precise PE or book value ratio. I have some idea of what company will look like in 5 years, and there is a disparity between that price and today's value.

CM: We don't know how to buy a stock based on ratios. We need to know how a company actually functions. Do you use a computer to screen anything?

WB: No I don't know how to. We don't really use screens but we are really screening everything. We look at it just as if someone offered us the whole thing, and what will it look like in five to ten years, and how sure of it we are and if it is in the price. There are a lot of businesses that we just don't know the answers to and feel that we can't foresee the future well enough. We have watched the auto business for 50 yrs. It is a very interesting business.

CM: BNSF will have a competitive advantage in 10 yrs. We don't know that about Apple or an oil company.

CM: People who are good at math look for numbers and think they can find an answer. You need to understand a company's competitive position, but it isn't that easy. It isn't math, you need to need to know the business.

WB: Not what I learned at Ben Graham. Not sure whether I would know how to manage money if I just had to look at the numbers.

CM: You would do it poorly. [laughter]

蛇足になりますが、ある石油会社が気になったことをきっかけに、石油業界を勉強しつづけています。今回引用したチャーリーの指摘は耳が痛いです。

蛇足その2です。昨日7日(金)は手持ちの日本株がそれなりの水準まで下落したため、わずかな金額ですが、売却してきた株を買い戻したり、買い増しをしました。割安と判断した指標はPERとPBRです。チャーリーの教えにことごとく背いているようで、微妙な思いがあります。

2013年5月16日木曜日

株式時価総額とGDPの比較グラフ

久しぶりにGDPの話題です。ウォーレン・バフェットが株式市場全体の値ごろ感をみるときに、株式時価総額がGNP(≒GDP)の何%に相当するか比較する話はよく知られています。個人的にもそのやりかたをまねして、ときおり日本にも当てはめています。以下の2か所のデータを使って算出しています。

・国民経済計算(GDP統計) (内閣府)

・東証株式時価総額 (東京証券取引所)

なお他取引所については、小規模だったり東証との重複上場があるため、個人的には考慮に入れていません。

さて、今回ご紹介する以下のWebサイトですが、自分が望んでいたそのものが掲載されており、とてもありがたいものでした。上述の計算結果が昔からのデータを使ってグラフ化されています。

Japan Market Capitalization to GDP (VectorGrader)

同サイトからグラフを2つほどお借りします。まず日本市場における株式時価総額対GDP(1970年以降)のグラフです(上部が時価総額対GDP、下部がおそらく日経平均)。

これをみて意外だったのは、日本市場では株価の高かった2000年当時よりも、直近のピークである2007年のほうが時価総額が大きかったことです。経済の裾野が広がったということでしょうか。

一方、アメリカ株式市場の状況(1950年以降)は次のグラフです(下部はおそらくS&P500)。

個人的な見解になりますが、この指標は厳密な指針を与えてくれるものとはとらえていません。「方向性がだいたい当たっている」程度のものと受けとめています。ちなみに2001年当時のウォーレンの発言では、GNP比で70-80%あたりを下回った時に買えばうまくいくとしています。

ご参考までに、以下の過去記事でもGDPについてふれています。コメント欄では、独自の分析結果をご紹介して頂いています。

GDP成長率と株式リターン率の関係(GMO)

(追記)コメント欄でご指摘を頂いています(NIGHT0878さんより)。2000年当時の日経平均は、銘柄入替え時に不連続性が生じているとのことです。

・国民経済計算(GDP統計) (内閣府)

・東証株式時価総額 (東京証券取引所)

なお他取引所については、小規模だったり東証との重複上場があるため、個人的には考慮に入れていません。

さて、今回ご紹介する以下のWebサイトですが、自分が望んでいたそのものが掲載されており、とてもありがたいものでした。上述の計算結果が昔からのデータを使ってグラフ化されています。

Japan Market Capitalization to GDP (VectorGrader)

同サイトからグラフを2つほどお借りします。まず日本市場における株式時価総額対GDP(1970年以降)のグラフです(上部が時価総額対GDP、下部がおそらく日経平均)。

これをみて意外だったのは、日本市場では株価の高かった2000年当時よりも、直近のピークである2007年のほうが時価総額が大きかったことです。経済の裾野が広がったということでしょうか。

一方、アメリカ株式市場の状況(1950年以降)は次のグラフです(下部はおそらくS&P500)。

個人的な見解になりますが、この指標は厳密な指針を与えてくれるものとはとらえていません。「方向性がだいたい当たっている」程度のものと受けとめています。ちなみに2001年当時のウォーレンの発言では、GNP比で70-80%あたりを下回った時に買えばうまくいくとしています。

ご参考までに、以下の過去記事でもGDPについてふれています。コメント欄では、独自の分析結果をご紹介して頂いています。

GDP成長率と株式リターン率の関係(GMO)

(追記)コメント欄でご指摘を頂いています(NIGHT0878さんより)。2000年当時の日経平均は、銘柄入替え時に不連続性が生じているとのことです。

2012年11月9日金曜日

EPSより大切な指標(ウォーレン・バフェット)

<追記>2017/7/17(月)

コメント欄で「匿名」さんからご指摘を受けたように、本記事では主題に関わる翻訳ミスがあったと判断しました。訂正箇所を具体的にまとめると、「ウォーレン・バフェットが主張した指標は"ROE的なもの"であって、当初の訳文にあげた"ROCE"ではない」となります。

本来であれば、訂正した訳文だけを残してその他の筋ちがいな文章(ROCEの説明など)を抹消すべきだとは思います。一方で、訂正に至るまでの経緯が見て取れることにも何らかの意味があると考え、ひとまずは翻訳ミスの言葉(抹消線付き)や当初の文章を残すこととしました。

企業分析の指標の一つとして、以前にROIC(投下資産利益率)をとりあげましたが(過去記事)、今回はそれと似ているようで少し違うROE(自己資本利益率)

なおウォーレンが営業上の成績をみるときには、以下の訳では「営業利益率」としていますが、保有証券を簿価評価した上で、期初の純資産を分母とする方式をあげています。これによって、証券の時価が変動するのを無視しています。

この基準によれば、1979年度の営業利益率は年初の純資産ベースで18.6%と、1978年度ほどではありませんが、十分な成績を収められました。EPSも20%ほど増加しましたが、この指標は注目すべきものではないとわたしどもは捉えています。1978年とくらべて1979年には使用できる資産が大幅に増加しました。しかしEPSは増加した一方で、資産を活かすという観点では前年ほどの成果は挙げられませんでした。EPSというものは、固定金利の利息を生む休眠口座や貯蓄債券ならば着実にあがります。得られた「利益」(ここでは利率)が継続的に元本に組み込まれて再投資されるからです。そのため「壊れた時計」でさえ、低配当率の成長株のようにみえてくるのです。

経営成績をはかる上で一番重要なのは、株主資本に対して高い利益率[ROE的な指標]高いROCE[使用資本利益率]が達成されていることであって(過度な借入や会計操作などは除きます)、EPSが一貫して上昇していくことではありません。もし経営者や金融アナリストが、EPSやその年次変化ばかりを気にする姿勢を変えれば、株主だけでなく一般の人にも、いろんなビジネスのことをうまく理解してもらえるだろう、とわたしどもは考えています。

On this basis, we had a reasonably good operating performance in 1979 ‐ but not quite as good as that of 1978 ‐ with operating earnings amounting to 18.6% of beginning net worth. Earnings per share, of course, increased somewhat (about 20%) but we regard this as an improper figure upon which to focus. We had substantially more capital to work within 1979 than in 1978, and our performance in utilizing that capital fell short of the earlier year, even though per‐share earnings rose. “Earnings per share” will rise constantly on a dormant savings account or on a U.S. Savings Bond bearing a fixed rate of return simply because “earnings” (the stated interest rate) are continuously plowed back and added to the capital base. Thus, even a “stopped clock” can look like a growth stock if the dividend payout ratio is low.

The primary test of managerial economic performance is the achievement of a high earnings rate on equity capital employed (without undue leverage, accounting gimmickry, etc.) and not the achievement of consistent gains in earnings per share. In our view, many businesses would be better understood by their shareholder owners, as well as the general public, if managements and financial analysts modified the primary emphasis they place upon earnings per share, and upon yearly changes in that figure.

ROICとROCEの計算式は、分子はほぼ共通の(営業利益) - (各種税金)ですが、分母が以下のように異なっています。(引用元: Wikipedia)

ROIC; (有利子負債) + (株主資本) - (業務上、余剰な現金及び資産) (2012/11/11訂正)

固定負債が少ない企業では、ROCEはROEに収束していくことになります。一方、ROEを向上させようとして株主資本の代わりに固定負債を増やしても、ROCEの値は変わりません。この2点については、ROCEはよくできた指標だと思います。ただし自己株式の取得が絡む場合、ひと工夫する必要があるかと思います。ROCEも、万能の指標というわけではありませんね。蛇足ですが、個人的にはROICとROCEを同じものだと思い込んでいました。

2012年9月12日水曜日

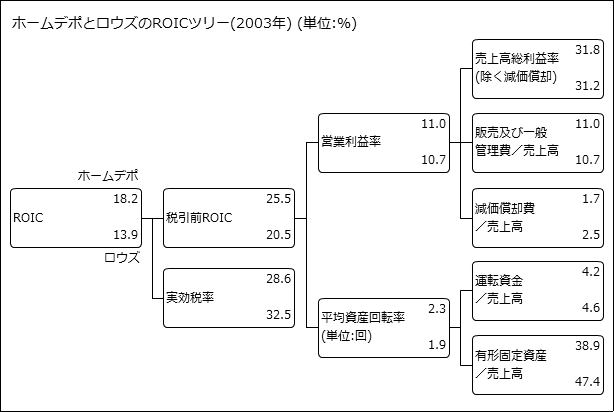

ROICを分解して競争優位性をさぐる

前回取り上げたルー・シンプソンの発言「資本収益率をチェックすると、実にいろいろなことがわかる」に導かれて、何かよい勉強材料はないかとさがしたところ、『企業価値評価 』という本に出会いました。最新である第5版の翻訳は刊行されたばかりですが、わたしが手にとっているのはひとつ前の『第4版

』という本に出会いました。最新である第5版の翻訳は刊行されたばかりですが、わたしが手にとっているのはひとつ前の『第4版 』のほうです。

』のほうです。

題名のとおり本書では、企業の価値がいくらなのか定量的に見積る方法論が紹介されています。マッキンゼーのメンバーが書いた本なので、最終的なねらいはクライアント企業の株価を上げることのように思われます。しかし内容はオーソドックスで、投資家にとっても参考になるものです。

今回ご紹介するのは、ROIC(Return On Invested Capital; 本書の訳は「投下資産利益率」)を分解した図です。例としてとりあげられた2社のROICは少なからず離れていますが、ROICをより細かな要素に分解することで、どのような要因によって差が生まれたのか浮き上がらせています。具体的にはホームセンター大手のホームデポとロウズの2社を比較し、「有形固定資産/売上高」の差異が大きいことを示しています。

(出典: 『企業価値評価 第4版』 p.218)

題名のとおり本書では、企業の価値がいくらなのか定量的に見積る方法論が紹介されています。マッキンゼーのメンバーが書いた本なので、最終的なねらいはクライアント企業の株価を上げることのように思われます。しかし内容はオーソドックスで、投資家にとっても参考になるものです。

今回ご紹介するのは、ROIC(Return On Invested Capital; 本書の訳は「投下資産利益率」)を分解した図です。例としてとりあげられた2社のROICは少なからず離れていますが、ROICをより細かな要素に分解することで、どのような要因によって差が生まれたのか浮き上がらせています。具体的にはホームセンター大手のホームデポとロウズの2社を比較し、「有形固定資産/売上高」の差異が大きいことを示しています。

(出典: 『企業価値評価 第4版』 p.218)

登録:

投稿 (Atom)