Walter Schloss Returns (Mr. Market Blog)

(このリンクは、いつもお世話になっている掲示板で取り上げられていたものです)

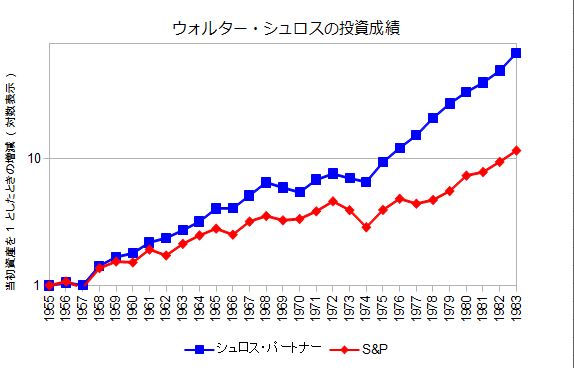

以下は、以前にとりあげたときのグラフを更新したものです。2000年から2002年にご注目ください。ITバブル後の下げ相場の時期です。

余談ですが、当時のわたしは株式投資を始めたころで、投資成績はS&P500と似たようなものでした。

1950年代にシュロス氏が自身の小ぶりなパートナーシップを始めるにあたって、彼はマンハッタンにあるバリュー志向の投資会社トゥイーディー・ブラウンの事務所に間借りさせてもらった。彼の居場所は正面ドアと冷水機の間だった。そこで座っていると、他の人が水を飲みにくるたびに身をかがめなければならなかった。やがて彼は小さな事務所へ引っ越した。息子のエドウィンがいっしょに働くようになるまで、秘書も事務員も会計係も雇わずに働きつづけた。

シュロス氏の調査資料には、企業の出す会計報告書と投資情報サービスを提供するバリューラインの古本が含まれていた。彼は企業の担当者に面会しに行ったり、経営陣と対談をすることはなかった。公開されている情報と自分の判断を頼りとしたのだ。(中略)

彼がそのようなすぐれた成績をあげられたのは、実直なやりかたをとことん貫いたおかげかもしれない。彼はまず、前年及びこの数年間の両方で新安値を更新した株式をさがした。次にその候補の中から、ビジネスモデルが単純で理解でき、負債が少なく、簿価より安い値段で取引されているものを選別した。また各企業の直近10~15年分の会計報告書を調べ、経営姿勢が欲深かったり倫理に反している企業、また失敗に終わりそうな製品を扱っている企業を除外した。

When Mr. Schloss decided to open his own modest partnership in the 1950s, he found space in the offices of Tweedy Browne, another value-oriented investing firm in Manhattan. He sat between the front door and the water cooler. If someone wanted a drink, Mr. Schloss had to scrunch up to let them by. He eventually moved into a modest office where he worked without a secretary, clerk or bookkeeper until he was joined by his son Edwin.

Mr. Schloss’s research materials included company financial reports and second-hand copies of Value Line, an investment advisory service. He didn’t travel to see companies or talk to management. Instead he relied on public information and his own judgment.

He generated these outstanding returns by methods that seem almost painfully straightforward. He started by looking for stocks trading at new lows both over the last year and over the last several years. He then winnowed down these candidates by looking for companies with simple, understandable business models and little debt that were trading below book value. He reviewed each company’s financial statements over the last 10 to 15 years and tried to avoid firms with greedy or unethical management and those with products that seemed likely to fail.

ウォルターはビジネススクールだけでなく、大学にも行きませんでした。1956年当時、彼の事務所にはファイル・キャビネットが1本あるだけでした。2002年までには、それが4本に増えました。ウォルターは、秘書や事務員、会計係を雇いませんでした。ただ、息子のエドウィンとだけ、仕事に勤しみました。エドウィンはノースカロライナ芸術学校の卒業生です。ウォルターとエドウィンは、インサイダー情報には一切近寄りませんでした。彼らが手にしたのは公開された情報だけで乏しいものでしたが、ウォルターがベン・グレアムのもとで働いていた頃に学んだ簡単な統計手法を使って株式を選び出しました。ウォルターとエドウィンは、1989年にOutstanding Investors Digest[バリュー投資家に好評のインタビュー誌]のインタビューで、こう聞かれています。「おふたりのやりかたを一言でいうと、どうなりますか」。エドウィンの答えは「株を安く買うようにつとめています」。モダンポートフォリオ理論、テクニカル分析、マクロ経済の見解、複雑なアルゴリズム。そういうのはお呼びじゃなかったのです。

Walter did not go to business school, or for that matter, college. His office contained one file cabinet in 1956; the number mushroomed to four by 2002. Walter worked without a secretary, clerk or bookkeeper, his only associate being his son, Edwin, a graduate of the North Carolina School of the Arts. Walter and Edwin never came within a mile of inside information. Indeed, they used “outside” information only sparingly, generally selecting securities by certain simple statistical methods Walter learned while working for Ben Graham. When Walter and Edwin were asked in 1989 by Outstanding Investors Digest, “How would you summarize your approach?” Edwin replied, “We try to buy stocks cheap.” So much for Modern Portfolio Theory, technical analysis, macroeconomic thoughts and complex algorithms.

(p.21)

「ウォルター・シュロスとは親しくお付き合いさせて頂いて、61年になります」

バフェットは昨日の声明の中で述べた。

「彼は飛びぬけた投資成績をあげてきましたが、それ以上に重要なのは、投資ビジネス界で誠実さのお手本になったことです。顧客が大きな利益をあげないかぎり、ウォルターはびた一文受けとりませんでした。つまり、固定報酬はとらずに、あがった利益の一部を受けとったのです。信義という面でも、投資能力に匹敵していました」

“Walter Schloss was a very close friend for 61 years,” Buffett said yesterday in a statement. “He had an extraordinary investment record, but even more important, he set an example for integrity in investment management. Walter never made a dime off of his investors unless they themselves made significant money. He charged no fixed fee at all and merely shared in their profits. His fiduciary sense was every bit the equal of his investment skills.”

「ふつうは割安になっている株を買うのが好みなので、もっと下がったときにもっと買うだけの度胸がいります」

1998年に開催されたGrant’s Interest Rate Observer協賛の会合で、シュロスは述べた。

「それこそが、ベン・グレアムがずっとやってきたことなんですよ」

“Basically we like to buy stocks which we feel are undervalued, and then we have to have the guts to buy more when they go down,” Schloss said at a 1998 conference sponsored by Grant’s Interest Rate Observer. “And that’s really the history of Ben Graham.”

エドウィン・シュロスはすでに引退しているが、昨日のインタビューで、父親の投資上の哲学と長命の間には因果関係があったのでは、と述べた。

「最近のマネー・マネージャーには、四半期ごとの決算も気になっている人が多いですね。朝の5時まで[眠れずに]爪をかじりあげているようですが、私の父は四半期決算の動きなんて、全然気にしてませんでした。だから、ぐっすり寝てましたよ」

Edwin Schloss, now retired, said yesterday in an interview that his father’s investing philosophy and longevity were probably related.

“A lot of money managers today worry about quarterly comparisons in earnings,” he said. “They’re up biting their fingernails until 5 in the morning. My dad never worried about quarterly comparisons. He slept well.”

1.価格こそが、価値をはかるのにいちばん大切な要因だ。

2.企業の価値を見定めよ。株式は企業の一部所有をあらわすものであって、ただの紙切れではないことを忘れないように。

3.企業価値を見定める際には、まずは簿価からみるようにしなさい。負債は株主資本とは等価ではない。

4.辛抱強くあれ。株価はすぐには上がらない。

5.聞いたうわさやちょっと株価が動いたからといって買わないこと。そういうのはプロにやらせておきなさい。それから、悪材料が出たからといって売らないように。

6.孤独を恐れずに、自分の判断を信じなさい。完全無欠とはいかないから、自分の考えのどこに弱点があるのか、さがしなさい。一段階下がったら買い、一段階上がったら売ること。

7.一度決めたら自分を信じる勇気を持ちなさい。

8.投資上の哲学をもって、それに従うようにしなさい。上に挙げたものは、うまくいくことを私自身が確かめてきたやりかたです。

9.売るときは急いで処分しすぎないこと。適正と思われる価格になったとき、例えば株価が50%あがると売って利益を確定するように言われるが、一度で売るのではなく、何度かに分けてもよい。売る前にはもう一度企業の価値を評価しなおして、簿価に見合った金額で売られているか確認すること。また相場の状況について、例えば、利回りが低くPERが高いか、歴史的に見て相場は高水準か、みんなは楽観的な様子か、といったことを知っておくこと。

10.株を買うときは、経験上、直近数年来での最安値あたりで買うのがよい。125[ドル]の高値をつけた株価が60[ドル]まで下がっていると魅力的に思えるが、3年間も意気消沈したあげく、結局20ドルで売ることになる。

11.利益に目をむけるよりも資産の割安度に目をむけて買うようにしなさい。短期で見ると利益は大きくふれるが、それにくらべて資産のほうはそれほどは変化しない。利益に注目するのであれば、企業についてより知りつくさなければならない。

12.尊敬する人の助言はきくこと。それをうのみにせよということではない。他でもない、[投資しているのは]自分のお金なのだから。ふつうは、増やすより維持するほうが大変なことを忘れないように。いったん大穴をあけてしまうと、とりもどすのは大変なのだから。

13.感情に任せて判断しないように注意しなさい。こわがったり傲慢な気持ちで株を売り買いするのは最悪のことだ。

14.複利の効果を忘れないように。年利12%で再投資しつづけると6年で2倍になる。これが72の法則で、72を利回りで割った答えが、当初資金が2倍になるのにかかる年数を示している。[72 ÷ 12 = 6年]

15.債券より株式を選ぶとよい。債券では利益が限られているし、インフレになると実質価値が減るからだ。

16.借金には注意せよ。仇となることがある。

1.Price is the most important factor to use in relation to value.

2.Try to establish the value of the company. Remember that a share of stock represents a part of a business and is not just a piece of paper.

3.Use the book value as a starting point to try and establish the value of the enterprise. Be sure that debt does not equal 100% of the equity. (Capital and surplus for the common stock).

4.Have patience. Stocks don't go up immediately.

5.Don't buy on tips or for a quick move. Let the professionals do that, if they can. Don't sell on bad news.

6.Don't be afraid to be a loner but be sure you are correct in your judgement. You can't be 100% certain but try to look for weaknesses in your thinking. Buy on a scale [down] and sell on a scale up.

7.Have the courage of your convictions once you have made a decision.

8.Have a philosophy of investment and try to follow it. The above is a way that I've found successful.

9.Don't be in too much of a hurry to sell. If the stock reaches a price that you think is a fair one, then you can sell but often because a stock a goes up say 50%, people say sell it and button up your profit. Before selling try to reevaluate the company again and see where the stock sells in relation to its book value. Be aware of the level of the stock market. Are yields low and P-E ratios high? Is the stock market historically high? Are people very optimistic etc?

10.When buying a stock, I find it helpful to buy near the low of the past few years. A stock may go as high as 125 and then decline to 60 and you think it attractive. Three years before the stock sold at 20 which shows there is some vulnerability to it.

11.Try to buy assets at a discount [rather] than to buy earnings. Earnings can change dramatically in a short time. Usually assets change slowly. One has to know much more about a company if one buys earnings.

12.Listen to suggestions from people you respect. This doesn't mean you have to accept them. Remember it's your money and generally it is harder to keep money than to make it. Once you lose a lot of money it is hard to make it back.

13.Try not to let your emotions affect your judgement. Fear and greed are probably the worst emotions to have in connection with the purchase and sale of stocks.

14.Remember the work of compounding. For example, if you can make 12% a year and reinvest the money back you will double your money in six years, taxes excluded. Remember the rule of 72. Your rate of return [divided] into 72 will tell you the number of years to double your money.

15.Prefer stocks over bonds. Bonds will limit your gains and inflation will limit your purchasing power.

16.Be careful of leverage. It can go against you.

ウォルター・シュロスは、そのての催しに声をかけられることがなかった。パートナーには登用されない、奉公あがりの雇われ人とみなされていたからだ。[パートナーの]ジェリー・ニューマンは他人に優しさをみせるような人間ではなかったが、それに輪をかけてシュロスを冷遇していた。そのため、シュロスには妻と2人の小さな子供がいたのだが、とうとう自ら辞めることを決意した。グレアムにはなかなか言い出せずにいたが、1955年の終わりに投資パートナーシップを立ち上げた。出資者から集めた資金はUS$100,000[=現在価値で約8,000万円]、バフェットがのちに認めるように、それらの出資者はエリス島で呼びかけたところに応じた者たちだった。

バフェットは、シュロスがグレアムのやり方をまねてうまくやるのは間違いないと思い、自身のファンドを立ち上げた心意気を賞賛した。ただ資金が少なすぎて家族を食わせてやれないのではとウォルターのことを心配したが、それでもバフェットは自分の資金をシュロスのパートナーシップにすこしも出資しなかった。グレアム・ニューマン[・パートナーシップ]に出資しなかったのと同じように、自分のお金を他人に投資してもらうなど論外だったからだ。

Walter Schloss was not invited to events like these. He had been pigeonholed as a journeyman employee who would never rise to partnership. Jerry Newman, who rarely bothered to be kind to anyone, treated Schloss with more than his usual contempt, so Schloss, married with two young children, decided to strike out on his own. It took him a while to get up the nerve to tell Graham, but by the end of 1955 he had started his own investment partnership, funded with

$100,000 raised from a group of partners whose names, as Buffett later put it, “were straight from a roll call at Ellis island."

Buffett was certain that Schloss could apply Graham’s methods successfully and admired him for having the guts to set up his own firm. Though he worried that “Big Walter” was starting out with so little capital that he would not be able to feed his family. Buffett put not a dime of his own money into Schloss’s partnership, just as he had not invested in Graham-Newman. It would be unthinkable for Warren Buffet to let someone else invest his money.

(p.197)