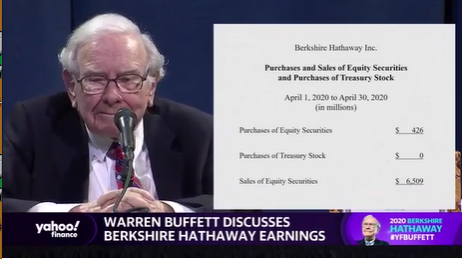

<ウォーレン・バフェット> そうしたのは基本的に、だれかが目標価格を変更したり、今期の利益予想を変更したことで、「株式市場は下落するか、今の状態で進むだろう」と考えるようになったからではありません。「企業の価値を評価する際に自分がまちがっていた」と判断したからです。それは原因が究明できる失敗でした。株式を買ったときには、確率で重みづけした上で決定をくだしました。そして航空業界にわたって投資していた時には、十分な見返りを得ていました。

最大手の航空会社4社を合算したとして、その10%ほどを購入しました。4月に実行[売却]したのは100%ではないですが、大手4社の10%を購入するために70億から80億ドルを支払いました。

当社としては、10億ドルほどの利益を得ていると考えていました。10億ドルの配当金を受け取ったわけではないですが、持分に相当する利益の額はおよそ10億ドルだとみなしていました。そしてある程度の期間でみれば、その金額を上回る年のほうが下回る年よりも多いだろうと予想していました。当然ながら周期的な変動はあるでしょうが、会社全体を買ったと想定して利益のことを考えていました。しかし当社はニューヨーク証券取引所で株式を買ったので、実際には4社全体の10%程度しか買えませんでした。わたしどもの心のなかでは、その事業を本当に保有しているかのように考えてきました。そして今回、わたし自身が事業のことをまちがってとらえていたという結果になりました。優秀なる4名のCEO諸氏が失敗をおかしたわけではありません。

(Warren Buffett 01:41:07)

And that's basically, that isn't because we thought the stock market was going to go down or anything of this order because somebody changes their target price or they change this year's earnings forecast. I just decided that I'd made a mistake in evaluating. That was an understandable mistake. It was a probability-weighted decision when we bought that, we were getting an attractive amount for our money when investing across the airlines business.

(Warren Buffett 01:41:43)

So we bought roughly 10% of the four largest airlines, and we probably... This is not 100% of what we did in April, but we probably paid $7 or $8 billion and then somewhere between $7 and $8 billion to own 10-

(Warren Buffett 01:42:03)

And somewhere between seven and eight billion to own 10% of the four large companies in the airline business, and we felt for that, we were getting a billion dollars roughly of earnings. Now we weren't getting a billion dollars of dividends, but we felt our share of the underlying earnings was a billion dollars and we felt that that number was more likely to go up than down over a period of time. It would be cyclical obviously, but it was as if we bought the whole company. But we bought it through the New York Stock Exchange, and we can only effectively buy 10% roughly of the four. And we treat it mentally exactly as if we were buying a business. And it turned out I was wrong about that business because of something that was not in any way the fault of four excellent CEOs.

今回の発言で個人的に注目したのは、チャーリー・マンガーの指摘を裏付ける箇所でした。今となっては基本的なことですが、それでも事実が確認できるというのはうれしいことですね。

・反射的に、にょきにょきと枝をのばす(チャーリー・マンガー)