<成長性>

それではここで、予想成長率を10%から7%へと低下させてみよう。なお、基準年の利益を100ドルとしている。

今期末の予想利益 PER 利益成長率 変更前 変更後 変更前 変更後 10% → 7% $110 $107 32.3 24.9

注目すべき点は、利益成長率が2.7%しか低下していないのに、そこから保証されるPER倍率は激しく急落して、22.9%も減少している点だ。投資家というものはPER倍率を算出する際に、現在の株価と来年[つまり今期末]の利益を使うことが多い。その結果、「次の利益はわずかな変化にとどまるようだが、それと比較すると市場は過剰に反応している」と思いこむことがある。しかし、PER倍率が大きく下落したように見えても、成長の足取りに対する期待がしぼんでしまえば、それは完全に正当化される。

(中略)

上述した計算は、バフェットが指摘した次のことを裏付けている。「価値(バリュー)を求める計算には、成長(グロース)という変数を必ず含んでいる。その変数は計算結果に対して、『軽微』以上『甚大』以下の影響を及ぼす」。資本コスト程度のリターンしか得られない事業では、価値を求める上で成長性はほとんど違いをもたらさない。しかし、投下資本に対して高いリターンをあげる事業では、成長性は価値を大きく増大させる。

Growth. Let’s start by reducing the growth rate from 10 percent to 7 percent. We’ll assume the base year earnings are $100.

Next year’s earnings P/E Growth Before After Before After 10% → 7% $110 $107 32.3 24.9

Note that the change in growth reduces next year’s earnings by only 2.7 percent, but that the warranted P/E multiple drops a more precipitous 22.9 percent. Investors often calculate the P/E multiple using the current price and next year’s earnings. As a result, they sometimes believe that the market overreacts to what appear to be modest changes in the near-term earnings. But if expectations for the trajectory of growth really do shift down, the large apparent drop in the P/E multiple is completely justified.

(snip)

This calculation substantiates Buffett’s point that, “Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous.” Growth makes little difference for businesses that earn a return close to the cost of capital but is a huge amplifier of value for high-return businesses.

2020年7月2日木曜日

企業の成長性と価値評価の関係(中)(マイケル・モーブッシン)

マイケル・モーブッシンのエッセイをもう少し取り上げます。今回の文章では、前回分の投稿で取り上げた割引キャッシュフロー・モデルを使い、事業の予想成長率が低下したときの価値評価をみています。(日本語は拙訳)

2020年7月1日水曜日

2020年バークシャー株主総会(36)欲望という名の電車

バークシャー・ハサウェイの株主総会より、ここからは今年3月に金融市場で起こっていた状況をウォーレン・バフェットが語ってくれます。前回分の投稿はこちらです。(日本語は拙訳)

<ウォーレン・バフェット> ですから、わたしどもがバークシャーに望んでいる位置とは..、『欲望という名の電車』に登場するブランチ・デュボアを覚えておられますか。多くの方が生まれるよりもずっと前の作品ですね。しかし彼女は「あの人たちを望んではいない」と言いました。ブランチの場合、「私はいつも他人のやさしさを頼りにしてきた」と言っていましたが、当社は友人の好意に頼りたいとは考えていません。なぜならば、資金がほとんど止まってしまう時期というものがあるからです。おもしろいことに、そういった例がひとつありました。もちろん2008年から2009年のことです。

しかし今年の3月23日の前日あるいは前々日には、それと非常に近い状況になりました。投資適格の諸企業が市場から実質的に締め出されようとしていたのです。ところが幸運なことに、その状況を連銀が把握していました。

米国じゅうの企業のCFOは株主資本の最大化をある種問われつづけてきたので、ある程度の資金は社債によって調達していました。なぜなら非常に安上がりな上に、銀行からの融資枠などが用意されていたからです。そのため多くの企業において、債務が相当な水準まで漸増していました。

当然ながら彼らは市場で起こったこと、特に株式市場の様子を知って縮みあがりました。そして、融資枠から引き出そうと殺到したのです。融資枠の期間を延長しようとしていた者たちはそのことに驚き、非常に神経質になりました。そして3月中旬に資金貸出要求が殺到したことで、それを受け入れるウォール街の余力は限界まで収縮しました。そしてついには各種市場を監視していた連銀が、非常に大きな行動をとるべきだと決断したのです。

(Warren Buffett 01:32:44)

So we want to be in a position at Berkshire where... Well, you remember Blanche DuBois in A Streetcar Named Desire - That goes back before many of you. But she said she didn't want them. In Blanche's case, she said that she depended on the kindness of strangers. And we don't want to be dependent on the kindness of friends even because there are times when money almost stops. And we had one of those, interestingly enough. We had it, of course, in 2008 and '09.

(Warren Buffett 01:33:32)

But right around in the day or two leading up to March 23rd, we came very close but fortunately we had a Federal Reserve that knew what to do, but money was... investment-grade companies were essentially going to be frozen out of the market.

(Warren Buffett 01:34:03)

CFOs all over the country had been taught to sort of maximize returns on equity capital, so they financed themselves to some extent through commercial paper because that was very cheap and it was backed up by bank lines and all of that. And they let the debt creep up quite a bit in many companies.

(Warren Buffett 01:34:22)

And then of course they had the hell scared out of them by what was happening in markets, particularly the equity markets. And so they rushed to draw down lines of credit. And that surprised the people who had extended those lines of credit; they got very nervous. And the capacity of Wall Street to absorb a rush to liquidity that was taking place in mid-March was strained to the limit to the point where the Federal Reserve, observing these markets, decided they had to move in a very big way.

2020年6月30日火曜日

2020年バークシャー株主総会(35)クレイトン大学対ビラノバ大学

バークシャー・ハサウェイの株主総会より、今回は現金比率の話題です。前回分の投稿はこちらです。(日本語は拙訳)

<ウォーレン・バフェット> それではこのスライドを..、いいえ、前のものに戻りましょう。ここに3月31日現在の当社が保有する現金及び米国債の正味保有残高を示しています。これをみて「現金と米国債を合わせて1,250億ドル、そしてさらに..」と思われるかもしれません。保有する株式は、少なくともその時点では1,800億ドルほどになっていました。

「1,800億ドルの株式に対して、ずいぶんと大量の米国債を保有しているものだ」と思われたかもしれません。しかし当社では実のところ、はるかに多額の株式を保有しています。多数の事業を保有しているからです。つまり非常に多くの子会社が発行した株式、その100%を保有しているわけです。わたしどもにしてみれば、それらは当社が保有する市場流通株ととてもよく似ています。当社はすべてを保有しているわけではなく、それらには呼び値が付いていません。

しかし、当社が保有する完全子会社の株式は何千億ドルにも達します。ですから、1,240億ドルになる現金の比率は40%ほどではなく、それよりもはるかに低い割合にとどまっています。さらにわたしどもは、常に大量の現金を手元に残すようにしています。これは、あらゆる事態に備えるためです。たとえば911が再来したり、第一次世界大戦のときのように株式市場が閉場されたり、といった事態です。その戦争は起こらないと思いますが、しかし今年の1月にクレイトン対ビラノバの[バスケットボールの]試合を観ていた時点では、このようなパンデミックも起こらないだろうと思っていました。[クレイトン大学の所在地はオマハ]

(Warren Buffett 01:31:07)

Now, I show on the slide that's up, I show our... Well, let's go back one. Yeah. I show our net, our cash and Treasury bill position on March 31st. And you might look at that and say, "Well, you've got $125 billion or so in cash and Treasury bills. And you've got..." At least at that point, we had about, I don't know, $180 billion or so in equities.

(Warren Buffett 01:31:43)

And you can say, "Well, that's a huge position to have in Treasury bills versus just $180 billion in equities." But we really have far more than that in equities because we own a lot of businesses. We own 100% of the stock of a great many businesses, which to us are very similar to the marketable stocks we own. We just don't own them all. They don't have a quote on them.

(Warren Buffett 01:32:05)

But we have hundreds of billions of wholly owned businesses. So our $124 billion is not some 40% or so cash positions, it's far less than that. And we will always keep plenty of cash on hand, and for any circumstances, with a 9/11 comes along, if the stock market is closed, as it was in World War I - it's not going to be, but I didn't think we were going to be having a pandemic when I watched that Creighton-Villanova game in January either.

2020年6月29日月曜日

2020年バークシャー株主総会(34)バークシャー・ハサウェイの基本原理

バークシャー・ハサウェイの株主総会より、ウォーレン・バフェットが財務にこだわる理由の一端を説明しています。3月の株価急落で目立った動きをみせなかったことに対して批判する意見もありますが、一株主としてはウォーレンやチャーリーの保守的な姿勢を支持します。前回分の投稿はこちらです。(日本語は拙訳)

<ウォーレン・バフェット> しかし利益がある程度減少したとしても、それらの事業は基本的に現金を生み出してくれます。そして2枚目のスライドに進みますが、バークシャーではきわめて強固な基盤を維持しています。これからも常にそれを守っていきますが、当社は単にそれを基本な方針としています。当社では一般の人たちと保険契約を結んでいます。ある程度は専門に特化しており、業界のリーダーでもあります。主たる事業ではないものの、定期金賠償商品も販売しています。たとえばだれかがひどい事故に遭ったとき、たいていは自動車事故ですが、10年から50年間などの期間にわたって援助が必要になります。それがこの商品です。

被害者の家族や弁護士は十分に賢明なようです。かれらの医療上の意図や費用やその他もろもろへ応じるために、巨額の一時金として受け取るよりも、基本的には当人が生涯にわたって支払いを受ける形態を選んでいます。当社の規模は巨大です。非常にたくさんの人たちが、実質的に当社と契約を結んでいます。当社はそれに従って、彼らが健康的な生活を送るための資金を支払っています。それはたとえば50年あるいはもっと先の未来まで続くかもしれません。

ですから、わたしとしてはいかなる状況においても、そのような人たちのお金を使って危険な賭けに臨むつもりはありません。チャーリーもそうですが、わたしどもはパートナーシップを運営するところから始めて、ここまでやってきました。わたしがパートナーシップを始めたのは1956年で、実際に7名の親族あるいは同等の人たちを募りました。6年後にはチャーリーも同じように始めました。どちらもそうだと思いますが、少なくともわたしは違いますし、チャーリーもほぼ間違いないと思いますが、どちらも機関投資家をパートナーに招くことは一切ありませんでした。

つまり、わたしどもが他人から預かった資金というのは、全額が個人からのものでした。実際に顔のある人物や集まりだったり、顔を持った資金でした(笑)。そのためわたしどもは、基本的に彼らの受託者たる仕事をしているのだと、いつも感じていました。果たすべき仕事という点で、それなりに賢明な受託者でありたいと望んでいました。しかし「受託者」という観点は非常に重要でした。そのことは、定期金賠償を受ける人たちにおいても重要ですし、どの位置にいる人にとっても重要です。しかし契約者に至っては非常に重要です。ですからわたしどもは、常に強固な財務のもとで事業を運営するようにしています。

(Warrren Buffett 01:28:13)

But basically these businesses will produce cash even though their earnings decline somewhat. And if we'll go to part two, at Berkshire, we keep ourselves in an extraordinary strong position. We'll always do that - that's just fundamental. We insure people. We're a specialist to some extent and a leader. It's not our main business, but we sell structured settlements. That means somebody gets in a terrible accident, usually an auto accident, and they're going to require care for 10, 30, 50 years.

(Warrren Buffett 01:29:03)

And their family or their lawyer is wise enough, in our view, to rather than take some big cash settlement to essentially arrange to have money paid over the lifetime of the individual to take care of their medical wills, bills, or whatever it may be. And we're large. We've got many, many, many people that in effect have staked their well-being on the promises of Berkshire to take care of them for, like I say, I mean, 50 years or longer into the future.

(Warrren Buffett 01:29:42)

And, now, I would never take real chances with money, of other people's money under any circumstances. Both Charlie and I come from a background where we ran partnerships. I started mine in 1956 for really seven either actual family members or the equivalent. And Charlie did the same thing six years later. And we never, neither one of us, I think, I know I didn't, and I'm virtually certain the same is true of Charlie, neither one of us ever had a single institution investment with us.

(Warren Buffett 01:30:23)

I mean, every single bit of money we managed for other people was from individuals, people with faces attached to them, or entities, or money with faces attached to them. So we've always felt that our job is basically that of a trustee, and hopefully a reasonably smart trustee in terms of what we were trying to accomplish. But the trustee aspect has been very important. And it's true for the people with the structured settlements. It's true for up and down the line. But it's true for the owners very much too. So we always operate from a position of strength.

2020年6月28日日曜日

企業の成長性と価値評価の関係(前補)(マイケル・モーブッシン)

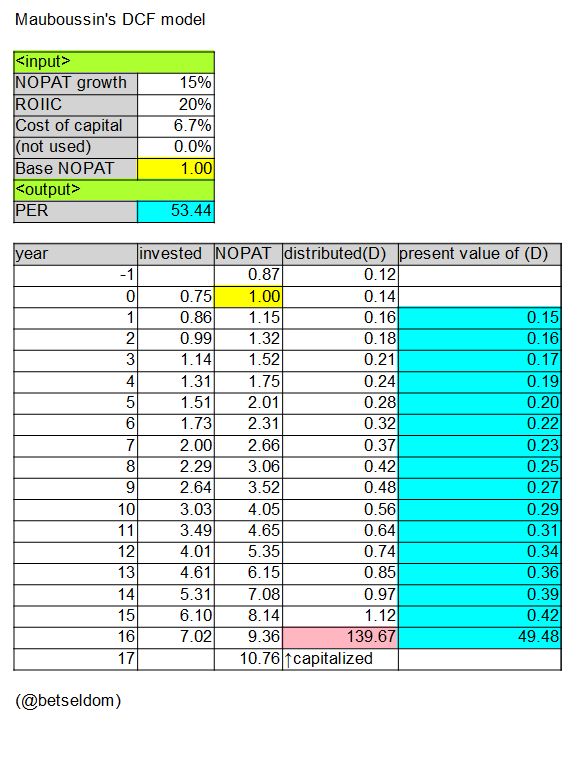

マイケル・モーブッシンに関する前回分の投稿で、コメント欄にてご質問がありました。「計算結果のPERが合わない」とのお問い合わせでしたが、今回の投稿はその返答になります。以下の図は、前回分投稿の内容に基づいてわたしが作成したスプレッドシートです。NOPAT成長率が10%と15%の2つの例を計算して、それぞれ掲載しています。

どちらの図でも出典元のエッセイで示されていたPERの数字(32.3および52.2)と合致していませんが、おおよそ合っていると勝手に判断して、それ以上は深入りしていません(計算途中の端数まるめ処理を調整するなど)。単純なモデルですが冷静にながめてみると、当たり前のことが数値になって現れており、ふだんの価値評価プロセスを見直す材料になりそうです。

(NOPAT成長率が10%の場合)

")

(NOPAT成長率が15%の場合)

どちらの図でも出典元のエッセイで示されていたPERの数字(32.3および52.2)と合致していませんが、おおよそ合っていると勝手に判断して、それ以上は深入りしていません(計算途中の端数まるめ処理を調整するなど)。単純なモデルですが冷静にながめてみると、当たり前のことが数値になって現れており、ふだんの価値評価プロセスを見直す材料になりそうです。

(NOPAT成長率が10%の場合)

")

(NOPAT成長率が15%の場合)

登録:

コメント (Atom)