<ウォーレン・バフェット> 飛行機が多すぎるのです。数か月前に発注が下されて合意がなされたときには、そのような状況ではありませんでした。しかし航空会社にとって世界は変化してしまいました。彼らにはうまくいってほしいと思いますが、しかし航空会社は当社が保有する事業のひとつでした。当社が直接保有している企業のなかには、これから大きな傷を負うことになる会社もあります。例のウィルスはバークシャーの資金を奪っていきます。「株式だから資金が減る」という意味ではありません。それは事業によってさまざまです。たとえばXYZという会社の株を保有していて、つまり一事業として保有しており、その会社を気に入っているとします。しかしXYZ社の株価が20%あるいは40%下落しても、その状況で損をしたとは感じません。一方で、今回実際に航空会社に起こったという意味では、まるで100%保有している会社であるかのように、痛手を受けたと感じました。

これで、航空会社株の売却に関する話はおわりです。他とくらべると少額なほうでしたが、この売却は今後の市場を予想した上で行ったわけではないことを、株主のみなさんにはよく理解していただきたいと思います。バークシャーの状況について、ざっとお話しできたかと思います。それではここからは、本総会における公式の議事を進めます。それらが済んだ後に、ベッキーの手元に質問がいろいろと寄せられていれば、質疑応答の時間を十分に用意してありますので、そちらで取りあげます。なお、公式の議事を進める間は興味津々な内容ということはありません。ですから、今ごらんになっている場所からご自由に離れてくださってかまいません。ベッキーに質問を送りたい方は、画面上に彼女の連絡先を掲げておきますので、ごらんください。サンドウィッチなどをこしらえるというのであれば、わたしどもは先に進んでおります。あるいは、公式議事をごらんになってもらってもかまいません。それでは始めましょう。長くはかかりません。その後に、質疑応答の部へ進みます。

(スピーチの部、おわり)

(Warren Buffett 01:45:26)

So you've got too many planes, but it didn't look that way when the orders were placed a few months ago, when arrangements were made. But the world changed for airlines and I wish them well, but it's one of the businesses we have. We have businesses we own directly that are going to be hurt significantly. The virus will cost Berkshire money. It doesn't cost money because of our stock. And various other businesses moves around. I mean, if XYZ, which say is one of our holdings and we own it as a business and we liked the business. The stock was down 20 or 30 or 40%. We don't feel we're poor in that situation. We felt we were poor in terms of what actually happened to those airline businesses just as if we don't a hundred percent of them. [as if we'd owned?]

(Warren Buffett 01:46:23)

So that explains those sales, which are relatively minor, but I want to make sure that nobody thinks that involves a market prediction. And that pretty well wraps it up for Berkshire. So now we move into the formal part of the meeting, which will be followed by a fairly extended question and answer period if there are a lot of questions with Becky. And while we're doing this formal part of the meeting, it's not too exciting. So feel free to leave whatever you're viewing this through, and if you want to send questions to Becky, we'll keep her contact information up on the screen. Or if you want to fix yourself a sandwich or do anything else, we will now move... Or you can pay attention to the formal part of the meeting. But we will do this, and it won't take too long, and then we will move on to the question and answer meeting.

2020年7月9日木曜日

2020年バークシャー株主総会(42)株式市場予測に基づいた売却ではない

バークシャー・ハサウェイの株主総会より、今回でウォーレン・バフェットのスピーチはおわりです。前回分の投稿はこちらです。(日本語は拙訳)

2020年7月8日水曜日

2020年バークシャー株主総会(41)航空業界に残る問題

バークシャー・ハサウェイの株主総会より、航空業界への投資を引き揚げた件についてです。前回分の投稿はこちらです。(日本語は拙訳)

本当のところ、航空会社のCEOという仕事は楽しいものではありません。しかし当社が買ったどの会社もよく経営されていました。たくさんのことを適切に遂行していました。なんといっても難しい事業です。毎日何百万人もの人が関わっており、そのうちの1%の人にまずいことがあれば、ずいぶんと残念な気持ちになってしまいます。ですから、航空会社のCEOの座に就いている人をうらやましいと思ったことはありません。特に今回のような時期においては、なおさらです。基本的には「飛ぶな」と言われている業界です。わたしも「しばらくは飛行機禁止」と言われました。飛行が再開されるのを期待しております。ただし定期便ではないかもしれませんが、それは別の話題になりますね。わたしの思いこみかもしれませんし、そうであってほしいとは思いますが、航空業界は非常に大きく変化したと思います。4社のそれぞれが平均100億から120億ドル以上の借入れをすると予想されることを考えると、明らかに実状が変わってしまいました。

その借金は、一定の期間にわたって利益から返済しなければなりません。つまりそのようなことになれば、100億から120億ドルの損失になります。新株を売るか、新株予約権を売らざるを得ない事態も考えられます。それでは逆に悪くなってしまいます。飛行機を使う人が増えることで、2,3年後には旅客マイルが昨年の水準に戻るのかどうか、わたしには判断できません。そうなるかもしれないし、ならないかもしれません。航空会社自体にはまったく問題がないことがわかったとしても、わたしにとって業界の未来はずいぶんと曖昧なものになってしまいました。つまり今回は確率の低い事象が起こったわけです。そのことで特に旅行業界やホテル業界、クルーズ業界、テーマパーク業界が傷を負いましたが、特にひどいのが航空業界でした。しかし商売が7割から8割回復したとしても、航空業界には依然として問題が残ります。航空機が消えずに残っている点です。

(Warren Buffett 01:43:01)

I mean, believe me, no joy being a CEO of an airline, but the companies we bought are well managed. They did a lot of things right. It's a very, very, very difficult business because you're dealing with millions of people every day, and if something goes wrong for 1% of them, they are very unhappy. So I don't envy anybody the job of being CEO of an airline, but I particularly don't enjoy being it in a period like this, where essentially nobody... People have been told basically not to fly. I've been told not to fly for a while. I'm looking forward to flying them. May not fly commercial, but that's another question. The airline business, and I may be wrong and I hope I'm wrong, but I think it changed in a very major way, and it's obviously changed in the fact that there're four companies are each going to borrow perhaps an average of at least 10 or 12 billion each.

(Warren Buffett 01:44:11)

You have to pay that back out of earnings over some period of time. I mean, you're 10 or $12 billion worse off if that happens. And of course in some cases they're having to sell stock or sell the right to buy a stock at these prices. And that takes away from the upside down. And I don't know whether it's two or three years from now that as many people will fly as many passenger miles as they did last year. They may and they may not, but the future is much less clear to me, [inaudible 00:02:52], how the business will turn out through absolutely no fault of the airlines themselves. That's something that was a low probability event happened, and it happened to hurt particularly the travel business, the hotel business, cruise business, the theme park business, but the airline business in particular. And of course the airline business has the problem that if the business comes back 70% or 80%, the aircraft don't disappear.

2020年7月7日火曜日

2020年バークシャー株主総会(40)わたしの間違いでした

バークシャー・ハサウェイの株主総会より、ウォーレン・バフェットの実質的な謝罪会見です。 このように誠実な態度を示せるリーダーのもとでは、真っ当な文化が育まれていると期待したいものです。前回分の投稿はこちらです。(日本語は拙訳)

今回の発言で個人的に注目したのは、チャーリー・マンガーの指摘を裏付ける箇所でした。今となっては基本的なことですが、それでも事実が確認できるというのはうれしいことですね。

・反射的に、にょきにょきと枝をのばす(チャーリー・マンガー)

<ウォーレン・バフェット> そうしたのは基本的に、だれかが目標価格を変更したり、今期の利益予想を変更したことで、「株式市場は下落するか、今の状態で進むだろう」と考えるようになったからではありません。「企業の価値を評価する際に自分がまちがっていた」と判断したからです。それは原因が究明できる失敗でした。株式を買ったときには、確率で重みづけした上で決定をくだしました。そして航空業界にわたって投資していた時には、十分な見返りを得ていました。

最大手の航空会社4社を合算したとして、その10%ほどを購入しました。4月に実行[売却]したのは100%ではないですが、大手4社の10%を購入するために70億から80億ドルを支払いました。

当社としては、10億ドルほどの利益を得ていると考えていました。10億ドルの配当金を受け取ったわけではないですが、持分に相当する利益の額はおよそ10億ドルだとみなしていました。そしてある程度の期間でみれば、その金額を上回る年のほうが下回る年よりも多いだろうと予想していました。当然ながら周期的な変動はあるでしょうが、会社全体を買ったと想定して利益のことを考えていました。しかし当社はニューヨーク証券取引所で株式を買ったので、実際には4社全体の10%程度しか買えませんでした。わたしどもの心のなかでは、その事業を本当に保有しているかのように考えてきました。そして今回、わたし自身が事業のことをまちがってとらえていたという結果になりました。優秀なる4名のCEO諸氏が失敗をおかしたわけではありません。

(Warren Buffett 01:41:07)

And that's basically, that isn't because we thought the stock market was going to go down or anything of this order because somebody changes their target price or they change this year's earnings forecast. I just decided that I'd made a mistake in evaluating. That was an understandable mistake. It was a probability-weighted decision when we bought that, we were getting an attractive amount for our money when investing across the airlines business.

(Warren Buffett 01:41:43)

So we bought roughly 10% of the four largest airlines, and we probably... This is not 100% of what we did in April, but we probably paid $7 or $8 billion and then somewhere between $7 and $8 billion to own 10-

(Warren Buffett 01:42:03)

And somewhere between seven and eight billion to own 10% of the four large companies in the airline business, and we felt for that, we were getting a billion dollars roughly of earnings. Now we weren't getting a billion dollars of dividends, but we felt our share of the underlying earnings was a billion dollars and we felt that that number was more likely to go up than down over a period of time. It would be cyclical obviously, but it was as if we bought the whole company. But we bought it through the New York Stock Exchange, and we can only effectively buy 10% roughly of the four. And we treat it mentally exactly as if we were buying a business. And it turned out I was wrong about that business because of something that was not in any way the fault of four excellent CEOs.

今回の発言で個人的に注目したのは、チャーリー・マンガーの指摘を裏付ける箇所でした。今となっては基本的なことですが、それでも事実が確認できるというのはうれしいことですね。

・反射的に、にょきにょきと枝をのばす(チャーリー・マンガー)

2020年7月6日月曜日

企業の成長性と価値評価の関係(後)(マイケル・モーブッシン)

マイケル・モーブッシンのエッセイより、今回で最後です。「成長投資」という言葉を株主の立場からみつめなおす話題です。あっさりとした内容の文章に読めますが、企業へ長期的に投資をして大きな利益をあげる上で、この話題は核心になるものだと、個人的には考えています。前回分の投稿はこちらです。(日本語は拙訳)

ここでいったん、文中で登場する用語を説明する文章に移ります。「標準PER倍率(commodity P/E multiple)」という用語についてです。

以下、本文に戻ります。

<ROIIC>

さらにここからは、ROIICの予想値が変化するとどのような影響がでるのか見てみよう。NOPAT(税引後営業利益)成長率が10%と仮定した状況に戻って、異なるROIICを設定することで保証PER倍率がどうなるのか検討していく。

ROIIC. We now turn to seeing the impact of changing assumptions about ROIIC. We’ll revert back to our 10 percent baseline NOPAT growth and consider the warranted P/E multiples assuming different ROIICs.

ここでいったん、文中で登場する用語を説明する文章に移ります。「標準PER倍率(commodity P/E multiple)」という用語についてです。

標準PER倍率(commodity P/E multiple)の基礎的な例から始めよう。この値は「年あたり1ドルの利益を生み出すが、今後は新たな価値を創出しない永久債として扱うべきもの」に対して支払う金額の倍率である。これを求めるには、資本コストの逆数を乗算すればよい。たとえば資本コストが8%であれば、標準PER倍率は12.5になる(1 / 0.08 = 12.5)。

Let’s start with the basic example of the commodity P/E multiple. This is the multiple you should pay for $1 of earnings into perpetuity assuming no value creation. You calculate the multiple by taking the inverse of the cost of equity capital. For example, if the cost of equity is 8 percent, the commodity P/E multiple is 12.5 (1/.08 = 12.5).

以下、本文に戻ります。

図4にその結果を示す。この条件における標準PER倍率が14.9であることに留意してほしい[6.7%の逆数]。それでは考えを進めてみよう。ROIICは、予想成長率を達成するために資金をどれだけ投下すべきかを示している。ROIICが高ければ、成長に対する投資はそれほど必要ではない。つまり、株主に回すことのできる現金が多く残る。その反対にROIICが低いと、成長を果たすための資金が余計にかかり、株主用の現金が少なくなる。

バフェットは、成長することが「好影響になることもあるし、悪影響になることもある」と付け加えた。ROIICが資本コストを下回っていれば、成長は[価値に対して]悪影響を与える。そのような企業は1ドルの資本を費やすことで、1ドル未満の価値を手にいれるのだ。その場合、企業の成長が急速であるほど、より多くの財産が失われていくことになる。

上記の図は「ROIICが資本コスト6.7%に満たないと、株価のPER倍率が標準倍率を下回る」ことを示している。企業買収の例がこれに当てはまる。一般に買収を実現することで、買い手からすれば利益は増加するものの、[企業]価値は下落する。つまり「ROIICの低い投資を実施している企業は、株価倍率を標準倍率へ押し下げている」と、みなすことができるだろう。

Exhibit 4 shows the results. Recall that the commodity P/E is 14.9. Here’s the way to think about it: ROIIC tells you how much you have to invest to achieve an assumed growth rate. A high ROIIC means you don’t need to invest much to grow, which means there’s more cash left over for shareholders. A low ROIIC means you have to invest a lot of capital to grow, leaving little for the owners.

Buffett added that the impact of growth “can be negative as well as positive.” Growth is a negative when the ROIIC is below the cost of capital. In that case, a company is spending $1 worth of capital to attain less than $1 of value. The faster the company grows the more wealth it destroys.

The exhibit shows that an ROIIC below the cost of capital of 6.7 percent yields a P/E multiple below the commodity multiple. Acquisitions are again a case in point. For buyers, M&A deals commonly add to earnings growth but subtract from value. You can think of low-ROIIC investments as pushing down the P/E multiple of a company’s stock toward the commodity multiple.

2020年7月5日日曜日

2020年バークシャー株主総会(39)4月はずいぶん売りました

バークシャー・ハサウェイの株主総会より、FEDの救済をよそに、ウォーレン・バフェットが今回の危機に直面して取った行動について説明しています。前回分の投稿はこちらです。(日本語は拙訳)

<ウォーレン・バフェット> しかし、わたしどもはバークシャーで準備をしていました。あれほどまでに行動できる議長がFEDにいない場合を想定して、つねに備えてきました。わたしどもはあらゆることに備えたいと考えています。そのことが、現金や債券で1,240億ドル分を保有している説明の一部になっていると思います。ですから当社には、そのすべてが必要なわけではありません。

しかし当社は他人のやさしさのみならず、友人のやさしさにも頼りたくないと考えています。次のスライドは株式に関する行動についてですが、年初における資産の市場評価額は5,000億ドルに近かったので、その規模から考えてみれば小さな金額でした。購入した自社株は17億ドルでした。また株式の購入は売却を20億ドルほど上回りました。

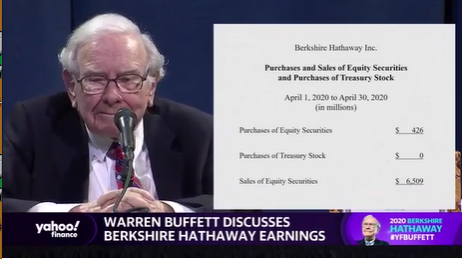

先ほどのスライドでみたように、営業利益は60億に近い50億ドル台でした。ですから第1四半期にはほとんど何もしていません。そしてスライドをもうひとつ加えましたが、これは通常公表していないものです。しかし、投資や株式についていつもよりお話しするのは、バークシャーが実際に行っていることを知ってほしいからです。それで4月はどうだったかと言いますと、正味60億ドルほどの証券を売却しました。

(Warren Buffett 01:39:16)

But we're prepared at Berkshire. We always prepare on the [ad 01:39:20], on the basis that maybe the Fed will not have a chairman that acts like that. And we really want to be prepared for anything. So that explains some of the $124 billion in cash and bills. We don't need it all.

(Warren Buffett 01:39:39)

But we never want to be dependent on not only the kindness of strangers but the kindness of friends. Now, in the next slide, we have the what we did in equities, and these numbers are tiny when you get right down to it. I mean, for having $500 billion or so in net worth and... I mean, not net worth, but in market value at the start of the year or something close to that. We bought in $1.7 billion of stock, and our purchases were a couple of billion more than our sales of equities.

(Warren Buffett 01:40:26)

But as you saw in the previous slide, we had operating earnings of $5, almost $6 billion. So we did very little in the first quarter. And then I've added in another figure, which I wouldn't normally present to you. But I want to be sure that if I'm talking to you about investments and stocks more than I usually have, I want you to know what Berkshire's actually doing. Now, you'll see in the month of April that we net sold $6 billion or so of securities.

登録:

投稿 (Atom)