<ウォーレン・バフェット> それではこのスライドを..、いいえ、前のものに戻りましょう。ここに3月31日現在の当社が保有する現金及び米国債の正味保有残高を示しています。これをみて「現金と米国債を合わせて1,250億ドル、そしてさらに..」と思われるかもしれません。保有する株式は、少なくともその時点では1,800億ドルほどになっていました。

「1,800億ドルの株式に対して、ずいぶんと大量の米国債を保有しているものだ」と思われたかもしれません。しかし当社では実のところ、はるかに多額の株式を保有しています。多数の事業を保有しているからです。つまり非常に多くの子会社が発行した株式、その100%を保有しているわけです。わたしどもにしてみれば、それらは当社が保有する市場流通株ととてもよく似ています。当社はすべてを保有しているわけではなく、それらには呼び値が付いていません。

しかし、当社が保有する完全子会社の株式は何千億ドルにも達します。ですから、1,240億ドルになる現金の比率は40%ほどではなく、それよりもはるかに低い割合にとどまっています。さらにわたしどもは、常に大量の現金を手元に残すようにしています。これは、あらゆる事態に備えるためです。たとえば911が再来したり、第一次世界大戦のときのように株式市場が閉場されたり、といった事態です。その戦争は起こらないと思いますが、しかし今年の1月にクレイトン対ビラノバの[バスケットボールの]試合を観ていた時点では、このようなパンデミックも起こらないだろうと思っていました。[クレイトン大学の所在地はオマハ]

(Warren Buffett 01:31:07)

Now, I show on the slide that's up, I show our... Well, let's go back one. Yeah. I show our net, our cash and Treasury bill position on March 31st. And you might look at that and say, "Well, you've got $125 billion or so in cash and Treasury bills. And you've got..." At least at that point, we had about, I don't know, $180 billion or so in equities.

(Warren Buffett 01:31:43)

And you can say, "Well, that's a huge position to have in Treasury bills versus just $180 billion in equities." But we really have far more than that in equities because we own a lot of businesses. We own 100% of the stock of a great many businesses, which to us are very similar to the marketable stocks we own. We just don't own them all. They don't have a quote on them.

(Warren Buffett 01:32:05)

But we have hundreds of billions of wholly owned businesses. So our $124 billion is not some 40% or so cash positions, it's far less than that. And we will always keep plenty of cash on hand, and for any circumstances, with a 9/11 comes along, if the stock market is closed, as it was in World War I - it's not going to be, but I didn't think we were going to be having a pandemic when I watched that Creighton-Villanova game in January either.

2020年6月30日火曜日

2020年バークシャー株主総会(35)クレイトン大学対ビラノバ大学

バークシャー・ハサウェイの株主総会より、今回は現金比率の話題です。前回分の投稿はこちらです。(日本語は拙訳)

2020年6月29日月曜日

2020年バークシャー株主総会(34)バークシャー・ハサウェイの基本原理

バークシャー・ハサウェイの株主総会より、ウォーレン・バフェットが財務にこだわる理由の一端を説明しています。3月の株価急落で目立った動きをみせなかったことに対して批判する意見もありますが、一株主としてはウォーレンやチャーリーの保守的な姿勢を支持します。前回分の投稿はこちらです。(日本語は拙訳)

<ウォーレン・バフェット> しかし利益がある程度減少したとしても、それらの事業は基本的に現金を生み出してくれます。そして2枚目のスライドに進みますが、バークシャーではきわめて強固な基盤を維持しています。これからも常にそれを守っていきますが、当社は単にそれを基本な方針としています。当社では一般の人たちと保険契約を結んでいます。ある程度は専門に特化しており、業界のリーダーでもあります。主たる事業ではないものの、定期金賠償商品も販売しています。たとえばだれかがひどい事故に遭ったとき、たいていは自動車事故ですが、10年から50年間などの期間にわたって援助が必要になります。それがこの商品です。

被害者の家族や弁護士は十分に賢明なようです。かれらの医療上の意図や費用やその他もろもろへ応じるために、巨額の一時金として受け取るよりも、基本的には当人が生涯にわたって支払いを受ける形態を選んでいます。当社の規模は巨大です。非常にたくさんの人たちが、実質的に当社と契約を結んでいます。当社はそれに従って、彼らが健康的な生活を送るための資金を支払っています。それはたとえば50年あるいはもっと先の未来まで続くかもしれません。

ですから、わたしとしてはいかなる状況においても、そのような人たちのお金を使って危険な賭けに臨むつもりはありません。チャーリーもそうですが、わたしどもはパートナーシップを運営するところから始めて、ここまでやってきました。わたしがパートナーシップを始めたのは1956年で、実際に7名の親族あるいは同等の人たちを募りました。6年後にはチャーリーも同じように始めました。どちらもそうだと思いますが、少なくともわたしは違いますし、チャーリーもほぼ間違いないと思いますが、どちらも機関投資家をパートナーに招くことは一切ありませんでした。

つまり、わたしどもが他人から預かった資金というのは、全額が個人からのものでした。実際に顔のある人物や集まりだったり、顔を持った資金でした(笑)。そのためわたしどもは、基本的に彼らの受託者たる仕事をしているのだと、いつも感じていました。果たすべき仕事という点で、それなりに賢明な受託者でありたいと望んでいました。しかし「受託者」という観点は非常に重要でした。そのことは、定期金賠償を受ける人たちにおいても重要ですし、どの位置にいる人にとっても重要です。しかし契約者に至っては非常に重要です。ですからわたしどもは、常に強固な財務のもとで事業を運営するようにしています。

(Warrren Buffett 01:28:13)

But basically these businesses will produce cash even though their earnings decline somewhat. And if we'll go to part two, at Berkshire, we keep ourselves in an extraordinary strong position. We'll always do that - that's just fundamental. We insure people. We're a specialist to some extent and a leader. It's not our main business, but we sell structured settlements. That means somebody gets in a terrible accident, usually an auto accident, and they're going to require care for 10, 30, 50 years.

(Warrren Buffett 01:29:03)

And their family or their lawyer is wise enough, in our view, to rather than take some big cash settlement to essentially arrange to have money paid over the lifetime of the individual to take care of their medical wills, bills, or whatever it may be. And we're large. We've got many, many, many people that in effect have staked their well-being on the promises of Berkshire to take care of them for, like I say, I mean, 50 years or longer into the future.

(Warrren Buffett 01:29:42)

And, now, I would never take real chances with money, of other people's money under any circumstances. Both Charlie and I come from a background where we ran partnerships. I started mine in 1956 for really seven either actual family members or the equivalent. And Charlie did the same thing six years later. And we never, neither one of us, I think, I know I didn't, and I'm virtually certain the same is true of Charlie, neither one of us ever had a single institution investment with us.

(Warren Buffett 01:30:23)

I mean, every single bit of money we managed for other people was from individuals, people with faces attached to them, or entities, or money with faces attached to them. So we've always felt that our job is basically that of a trustee, and hopefully a reasonably smart trustee in terms of what we were trying to accomplish. But the trustee aspect has been very important. And it's true for the people with the structured settlements. It's true for up and down the line. But it's true for the owners very much too. So we always operate from a position of strength.

2020年6月28日日曜日

企業の成長性と価値評価の関係(前補)(マイケル・モーブッシン)

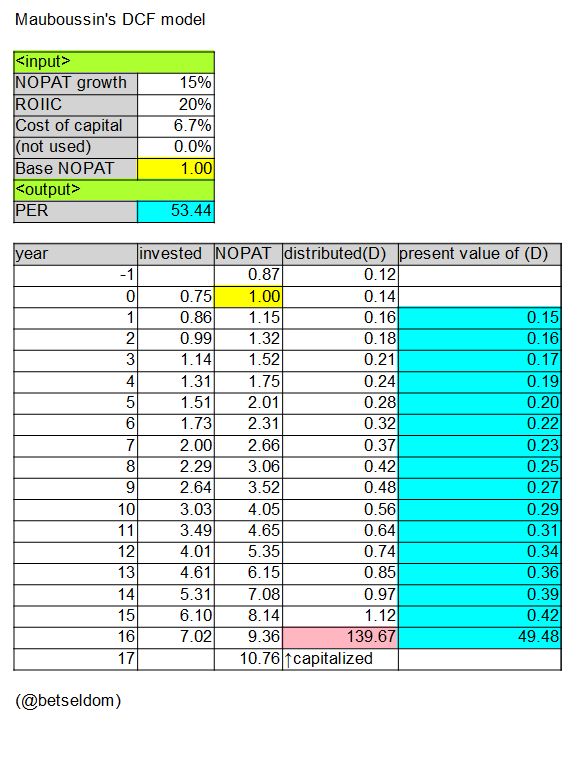

マイケル・モーブッシンに関する前回分の投稿で、コメント欄にてご質問がありました。「計算結果のPERが合わない」とのお問い合わせでしたが、今回の投稿はその返答になります。以下の図は、前回分投稿の内容に基づいてわたしが作成したスプレッドシートです。NOPAT成長率が10%と15%の2つの例を計算して、それぞれ掲載しています。

どちらの図でも出典元のエッセイで示されていたPERの数字(32.3および52.2)と合致していませんが、おおよそ合っていると勝手に判断して、それ以上は深入りしていません(計算途中の端数まるめ処理を調整するなど)。単純なモデルですが冷静にながめてみると、当たり前のことが数値になって現れており、ふだんの価値評価プロセスを見直す材料になりそうです。

(NOPAT成長率が10%の場合)

")

(NOPAT成長率が15%の場合)

どちらの図でも出典元のエッセイで示されていたPERの数字(32.3および52.2)と合致していませんが、おおよそ合っていると勝手に判断して、それ以上は深入りしていません(計算途中の端数まるめ処理を調整するなど)。単純なモデルですが冷静にながめてみると、当たり前のことが数値になって現れており、ふだんの価値評価プロセスを見直す材料になりそうです。

(NOPAT成長率が10%の場合)

")

(NOPAT成長率が15%の場合)

2020年6月27日土曜日

2020年バークシャー株主総会(33)第1四半期の概況報告

バークシャー・ハサウェイの株主総会より、今回からは今期業績の話題に入ります。前回分の投稿はこちらです。(日本語は拙訳)

<ウォーレン・バフェット> それではざっと見ていきましょう。ここにベッキー[・クイック。ウォーレンご指名の有名ニュースキャスター]の電子メール・アドレスがありますので、わたしが話したことなどについてご質問のある方は、電子メールでお知らせください。ベッキーは受け取った質問の山と格闘した末に、いくつかを選び出して順番を決めてくれるはずです。今回わたしが話したことであれば長くてもかまいませんので、遠慮なしに彼女へ送ってください。本総会が公式の部へ進行した間にも、彼女の電子メールアドレスは掲げておきます。

さてバークシャーの第1四半期について、ごく簡単にお話ししたいと思います。スライドはどちらでしたか。これですね。それでは営業利益についてです。[SECに提出した]10-Qでは詳細に触れているので、この場で時間を費やす必要はないのですが、第1四半期の営業利益は、来年度の予想を立てるという点では何の意味もない数字です。

米国経済がシャットダウンすることでどのような事態になるのか、わたしにはわかっていませんでした。何にせよ、それがうまくいくことはようやく理解しました。わたしたちは過ちをおかしたのかもしれません。そして、この話の最中やこれから後にも過ちをおかすことでしょう。しかしこの件で済んだことをとやかく言うつもりはありません。ほかの手段をとったときにどんな結果につながるのか、はっきりとわかる人などいないからです。

しかしわたしたちに言えるのは、ある程度の期間は、まちがいなく今年の残りの期間は、あるいは相当な期間にわたるかもしれませんが、それはだれにもわかりませんが、しかしウィルスが襲来しなかった場合とくらべると、当社の営業利益は大幅に減少します。つまりそういうことです。当社の事業には大きな傷を負ったものもあります。シャットダウンです。当社には事実上シャットダウンしていた事業がいくつかありました。

それ以外の事業におけるウィルスの影響は、もっと小さいものでした。当社の主力事業には、保険・BNSF鉄道・エネルギーの3つがあります。それらは当社の3強として他とは一定の差をつけており、かなりの地位を占めています。各社では償却費以上に資金を投資しています。そのため利益の一部は償却費とともに、増大する固定資産へと向けられることになります。

(Warrren Buffett 01:25:20)

So we will just now take a quick look. And I see we've got the Becky's email address. So if you have questions on what I've said or other things, you can email these questions. And she is back there probably sort of a madhouse trying to handle questions coming in and pick out the ones she's going to prioritize. But feel free to, anything I've talked about so far, to send a long to her, and we'll keep her address up when I later hold the formal part of the meeting too.

(Warrren Buffett 01:26:03)

Very briefly in terms of Berkshire, in the first quarter, if you'll put up... Do we have the slides on that? There we are. Our operating earnings were... And there's much more about this in the 10-Q, and it's really not worth spending any real time on. But the operating earnings for the first quarter have no meaning whatsoever in terms of forecasting what's going to happen the next year.

(Warrren Buffett 01:26:34)

And I don't know the consequences of shutting down the American economy. I know eventually it will work, whatever we do. We may make mistakes. We will make mistakes, and during this talk and later on, I'm not going to be second- guessing people on this because nobody knows for sure what any alternative action would produce or anything short.

(Warrren Buffett 01:27:06)

But what we do know is that for some period, certainly during the balance of the year, but it could go on a considerable period of time, who knows, but our operating earnings will be less, considerably less than if the virus hadn't come along. I mean, that's just it. It hurts some of our businesses a lot. I mean, you shut down. Some of our businesses effectively have been shut down.

(Warrren Buffett 01:27:41)

It affects others much less. Our three major businesses of insurance and the BNSF railroad, railroad and our energy business, those are our three largest by some margin. They're in a reasonably decent position. They will spend more than their depreciation. So some of the earnings will go, along with depreciation, will go toward increasing fixed assets.

2020年6月26日金曜日

企業の成長性と価値評価の関係(前)(マイケル・モーブッシン)

少し前の投稿で取り上げたマイケル・モーブッシンのエッセイでは、企業価値を評価する上での成長性や金利の影響について持論を展開しています。今回ご紹介するのは、PERのようなわかりやすい評価指標を使う上での注意を促すような文章です。(日本語は拙訳)

備考です。ROIICの具体的な計算例としては、米マクドナルド社がSECに提出した10-K中の文章が参考になりそうです。

・One-year return on incremental invested capital (ROIIC)

また本文中で取り上げられていた割引キャッシュフロー・モデルは、スプレッドシートでおおよそ再現できます。

計算式

それでは、PERが30台前半になるように入力値を調節した上で、割引キャッシュフロー・モデルを使って検討してみよう。 以下に、用語の定義と初期条件を記しておく。

・NOPAT(税引後営業利益)が年率10%で増加すると仮定した。NOPATとは、財務的な借入れに頼らないで企業があげる損益を示す金額である。

・ROIIC(増分投下資本利益率)が20%と仮定した。ROIICの定義は、今期と比較した来期NOPATの増分を、今期中に支出される投資額で除した割合である。たとえば、来期のNOPATが10ドル分増加すると見込まれ、今期中に50ドルを事業に投資するとき、ROIICは20%になる(=10/50)。ここで注意すべき点は、投資した資金の仕分け先が費用か資産かは問わない点である。ただし、若干の税効果は別とする。

・株主資本コストを6.7%と仮定した。これはアシュワス・ダモダラン[ニューヨーク大学スターン・スクールの教授]が2020年2月1日時点で見積もった値である。この指標は、想定されるリスクに対して投資家が期待しているリターンを測るものである。そのため無リスク金利1.5%に、株式リスク・プレミアムの推計値5.2%を加算した値となっている。話を単純にするため、対象企業の資本調達先は、株主からの出資だけとしている。なお、債券が加わっていると計算が若干やっかいになるが、筋書きが変わることはない。

・本モデルでは15年間で得られるキャッシュフローの価値を算出し、その後の期間については残存価値を見積もるために永久債として扱う。なお、NOPATを16年目にも計算している。これは15年目に実施された投資の成果を反映するためであり、さらにそれを株主資本コストを使って還元している。そうして得られた数値を現在価値へ割り引く。

以下に、このモデルにおける入力および出力値を示す。

(入力値)

NOPAT(税引後営業利益)の増加率: 10%

ROIIC(増分投下資本利益率): 20%

資本コスト: 6.7%

(出力値)

PER: 32.3

ここで増加率を15%にして他の値はそのままだと、以下のような結果が得られる。

(入力値)

NOPATの増加率: 15%

ROIIC: 20%

資本コスト: 6.7%

(出力値)

PER: 52.2

それでは次に、それらの初期条件を変化させることでPER倍率にどのような影響をもたらすのか確認しよう。[価値評価の際にPERのような]倍率を使っている投資家のほとんどは基礎的な仮定を熟慮していないため、概して彼らが予想する以上の変化があらわれる。

(つづく)

The Math

We start by calibrating our discounted cash flow model with inputs that yield a P/E multiple in the low 30s. Here are the definitions and the initial assumptions:

- We assume net operating profit after tax (NOPAT) will grow 10 percent per annum. NOPAT represents the cash profits a company would earn if it had no financial leverage.

- We assume a return on incremental invested capital (ROIIC) of 20 percent. ROIIC is defined as the change in NOPAT from this year to next year divided by this year’s investment. For example, if NOPAT grows by $10 next year and the company invests $50 this year, the ROIIC is 20 percent (10/50). Note that it does not matter if the investment is expensed or capitalized, save for some effect on taxes.

- We assume the cost of equity capital to be 6.7 percent, which was Aswath Damodaran’s estimate as of February 1, 2020. The cost of equity measures the return an investor expects to earn given the assumed risk. As such, the figure is the sum of the risk-free rate of 1.5 percent and an estimated equity risk premium of 5.2 percent. We assume the company is financed solely with equity for simplicity. Adding debt makes the calculations slightly more cumbersome but does not change the story.

- The model values explicit cash flows for 15 years after which it uses a perpetuity to estimate the residual value. Specifically, the model takes NOPAT in year 16, which reflects the benefit of the investment made in year 15, and capitalizes it by the cost of equity. That figure is then discounted to a present value.

Here’s a summary of the inputs and the output:

NOPAT growth: 10%

ROIIC: 20%

Cost of capital: 6.7%

→ P/E: 32.3

If we increase the growth rate to 15 percent and hold everything else constant, we get this result:

NOPAT growth: 15%

ROIIC: 20%

Cost of capital: 6.7%

→ P/E: 52.2

We will now change these assumptions to see what the impact is on the P/E multiple. Because most investors who use multiples do not contemplate foundational assumptions, the changes are larger than they generally expect.

備考です。ROIICの具体的な計算例としては、米マクドナルド社がSECに提出した10-K中の文章が参考になりそうです。

・One-year return on incremental invested capital (ROIIC)

また本文中で取り上げられていた割引キャッシュフロー・モデルは、スプレッドシートでおおよそ再現できます。

登録:

投稿 (Atom)